Modern developer teams don’t just integrate payments—they build entire products around them. Whether you’re orchestrating marketplace payouts, onboarding vendors at scale, or automating complex compliance workflows, the payment platform you choose becomes part of your core infrastructure. Legacy payment tools weren’t designed for this reality. They prioritize dashboards over APIs, manual processes over automation, and rigid workflows over extensibility.

API-first payment platforms flip that model. They expose payments, payouts, onboarding, and compliance as programmable building blocks, allowing engineers to move faster, reduce operational overhead, and ship financial features with the same rigor as the rest of their stack. This guide highlights the best API-first payment platforms for developer teams, focusing on real-world use cases like marketplace payouts, vendor onboarding, and global disbursements.

TLDR:

- API-first payment platforms let you trigger payouts programmatically with webhooks and idempotency

- Routable integrates in under 3 developer days with 14 webhook events and instant payment rails

- Stripe Connect works for marketplace teams already using Stripe but lacks deep ERP integration

- Hyperwallet offers global reach through PayPal but forces payees into PayPal-branded experiences

- Routable handles 220+ countries, automated tax compliance, and 99.8% accurate ERP sync in one system

What Are API-First Payment Platforms?

API-first payment infrastructure is built for developer teams who need to send programmatic disbursements at scale. Instead of manually processing payouts, these solutions let you push thousands of payouts to vendors and payees directly from your application using REST APIs.

The difference comes down to control and speed. Traditional payment orchestration tools are designed for finance teams processing vendor invoices and payouts with approval chains. API-first payment infrastructure gives your engineering team direct access to payment rails through code, so you can trigger payouts based on your business logic, whether that’s paying a driver after a delivery or disbursing royalties to hundreds of creators on a schedule.

You get webhook notifications when payments clear, idempotency to prevent duplicate transactions during network failures, and the ability to handle multiple payment methods across domestic and international rails, all without leaving your tech stack.

How We Ranked API Payment Platforms

We evaluated each solution based on criteria that matter when you’re running high-volume disbursements through code. The focus was on developer experience, programmatic control, and how well each system handles scale without adding headcount or stitching together multiple vendors.

API Capabilities and Developer Experience:

Integration speed matters when your engineering team needs to ship fast. We reviewed publicly available API documentation, sandbox availability, webhook implementations, and idempotency support. We looked for clear endpoint structures, error codes, and whether the API lets you create, schedule, search, and cancel payments programmatically.

Payout Speed and Rails:

When you’re competing on how fast your workforce gets paid, delivery speed directly impacts retention. We evaluated same-day ACH, instant payment options, and real-time tracking that lets payees see exactly when funds will arrive. We assessed domestic options (ACH with multiple speed tiers, wire, RTP, push-to-card, P2P) and international coverage (local rails, SWIFT, currency breadth, FX transparency).

Webhook Support and Status Tracking:

Real-time notifications when payments clear, fail, or get held let your application respond programmatically. We examined webhook event coverage, reliability, and whether payees can track their payment status through a self-service portal.

Compliance Automation:

Tax form collection (W-8/W-9), 1042-S/1099 filing, TIN validation, and watchlist screening need to happen during payee onboarding. We looked for systems that handle KYC, OFAC checks, and compliance holds without requiring manual intervention from your ops team.

ERP and Reconciliation Support:

Even API-first teams need clean books. We assessed bi-directional ERP sync capabilities, reconciliation automation, and whether the system removes manual data entry between your payment flows and accounting software.

These criteria reflect what breaks or scales for teams running disbursements as a core product feature. If payments are your competitive advantage, you need infrastructure that handles growth, gives developers control, and keeps payees happy.

Best Overall API-First Payment Infrastructure: Routable

Routable was built specifically for developer teams running mass payout operations. The REST API integrates in under 3 developer days and handles everything from creator royalties to driver disbursements without forcing you into invoice approval workflows designed for corporate AP.

You get 14 webhook events covering payment status, payee onboarding, and failure scenarios. Idempotency keys prevent duplicate payouts during network issues. External IDs let you tie every disbursement back to your application’s transaction records.

The API supports instant payments through RTP/FedNow, Same Day ACH, and Next Day ACH when speed matters for payee retention. For international disbursements, Routable covers 220+ countries in 140+ currencies with local rails and 30-50% savings on foreign exchange versus competitors.

Tax compliance runs automatically during payee onboarding. The platform collects W-8s and W-9s, validates TINs against IRS records, and handles 1042-S/1099 filing without manual ops work. Bank account verification and 6,000+ watchlist screening happen before the first payout goes out.

Finance teams get bi-directional ERP sync with NetSuite, Intacct, QuickBooks, and Xero at 99.8% accuracy. Payment data flows back automatically so month-end close doesn’t require manual reconciliation across thousands of transactions.

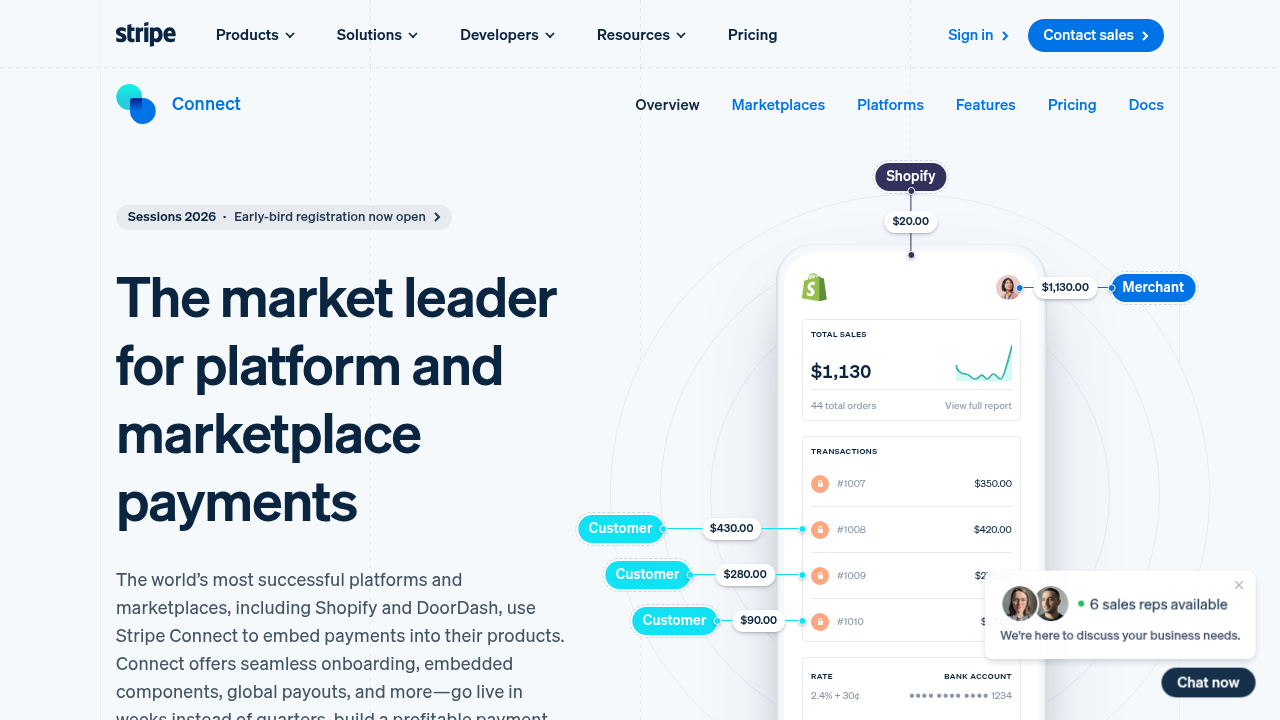

Stripe Connect

Stripe Connect works well for marketplace teams already using Stripe for payment acceptance who need to add seller or creator payouts. The platform gives you programmatic control over split payments, onboarding flows, and disbursement timing through their REST API. You can trigger payouts based on your business logic—like releasing funds to a seller after a buyer confirms delivery—and track payment status through webhook events.

The API supports instant payouts to debit cards and bank accounts, though availability varies by country and requires Stripe-issued cards for the fastest delivery. Standard ACH transfers take 2-3 business days. International coverage is more limited compared to dedicated mass payout platforms, and you’ll need to manage separate Stripe accounts for each market you operate in.

Where Stripe Connect falls short is deep ERP integration and compliance automation at scale. There’s no native bi-directional sync with NetSuite or Intacct, so reconciling thousands of marketplace transactions still requires manual work or custom middleware. Tax form collection works for 1099 filing, but you’re responsible for building the workflows that collect W-9s during seller onboarding and handle international tax documentation for cross-border payouts.

Hyperwallet

Hyperwallet (now part of PayPal) offers global payout infrastructure with coverage across 200+ countries and support for local payment methods through PayPal’s network. The platform provides REST API access for triggering mass disbursements to creators, gig workers, and marketplace sellers, with webhook notifications for payment status updates. You can programmatically create payees, initiate transfers, and handle multi-currency payouts through their API endpoints.

The main advantage is rapid international deployment—if your payees are already comfortable with PayPal, onboarding friction drops significantly. Hyperwallet supports local bank transfers, PayPal wallet deposits, and prepaid cards across most markets.

The biggest limitation is that Hyperwallet forces payees into PayPal-branded experiences rather than white-label flows. Your drivers, creators, or sellers see PayPal branding during onboarding and payment receipt, which dilutes your platform’s identity. There’s also no native ERP integration—you’ll need to build custom reconciliation workflows or use third-party middleware to sync payment data with NetSuite, Intacct, or QuickBooks. Tax compliance automation is limited compared to purpose-built mass payout platforms, requiring manual processes for W-8/W-9 collection and 1042-S/1099 filing at scale.

Checkbook

Checkbook offers a developer-friendly API for sending digital checks and ACH payments, positioning itself as a simple alternative to traditional payment processors. The platform provides straightforward REST API endpoints for creating and sending payments, with webhook support for tracking payment status. You can trigger payouts programmatically and give payees the option to receive funds via digital check, ACH transfer, or physical check.

The main appeal is simplicity—Checkbook’s API is easy to integrate for teams that need basic disbursement functionality without complex compliance workflows. Same Day ACH is available for faster payouts, and the platform handles basic payment tracking through their dashboard.

Where Checkbook falls short is scale and automation. The platform does not provide international coverage for payments made outside of the U.S. Tax compliance is entirely manual—you’re responsible for collecting W-8/W-9s, validating TINs, and handling 1042-S/1099 filing outside the platform. There’s no native ERP integration or automated payee onboarding flow with KYC or bank account validation. For marketplace or gig economy platforms processing thousands of monthly payouts, these gaps create operational bottlenecks that require additional headcount or third-party tools to manage.

Trolley

Trolley (formerly PaymentRails) provides API-first payout infrastructure designed for platforms managing high-volume disbursements to global payee networks. The platform offers REST API access with webhook notifications, letting you programmatically trigger payments to creators, sellers, and contractors across 210+ countries. You can create payees, initiate batch payments, and handle multi-currency disbursements through their API endpoints, with support for local bank transfers, PayPal, and various regional payment methods.

Trolley’s core strengths lie in international reach and tax compliance automation. The platform handles W‑8 and W‑9 collection during payee onboarding and supports 1042‑S and 1099 filing. However, it does not support Same-Day ACH or instant payment rails like RTP/FedNow. While webhooks allow real-time tracking of payment status, the API lacks idempotency key support, requiring engineering teams to implement safeguards against duplicate payments in case of network issues.

Where Trolley falls short is in ERP integration and white-label flexibility. There is no native bi-directional sync with NetSuite, Intacct, or QuickBooks, leaving finance teams to reconcile payments manually or build custom middleware. The payee portal offers limited branding customization, and CSV upload functionality is less robust than some competitors. Teams seeking a fully integrated, white-labeled payout experience with automated accounting sync will need additional development work to bridge these gaps.

Feature Comparison Table of API-First Payment Infrastructure

The differences between payment platforms become clear when you’re processing thousands of payouts through code. This comparison focuses on the technical capabilities that determine integration speed, payout reliability, and operational overhead: webhook support, idempotency, instant payment rails, ERP connectivity, and automated compliance workflows.

| Feature | Routable | Stripe Connect | Hyperwallet | Checkbook | Trolley |

|---|---|---|---|---|---|

| REST API | Yes | Yes | Yes | Yes | Yes |

| Webhook Support | Yes (14 events) | Yes | Yes | Yes | Yes |

| Idempotency Keys | Yes | Yes | Yes | Yes | No |

| Instant Payments | Yes (RTP/FedNow) | Limited | No | Yes (Push-to-card) | No |

| Same Day ACH | Yes | Limited | No | Yes | No |

| International Coverage (Countries) | 220+ | 40+ | 200+ | Limited – U.S. Only | 210+ |

| Native ERP Integration | Yes (4 ERPs) | No | No | No | No |

| Automated Tax Collection | Yes | Limited | Limited | No | Yes |

| Bank Account Validation | Yes | Yes | No | Yes | Limited |

| White-Label Payee Portal | Yes | No | No | No | Limited |

| CSV Upload Option | Yes | No | No | Yes | Yes |

Why Routable Is the Best API-First Payment Infrastructure for Developer Teams

Developer teams need payment infrastructure that eliminates context-switching between documentation and code while providing the payment rails, compliance automation, and ERP connectivity that finance teams rely on.

Nearly 90% of payment system providers cite efficiency gains as a key driver for API adoption, with APIs removing manual processes that slow down payouts and reconciliation.

Routable was built specifically for mass payout use cases, offering a developer-friendly REST API, instant payment options, automated tax workflows, and bi-directional accounting sync—all in a single integrated system. You get webhooks for every payment status change, idempotency keys to prevent duplicate disbursements, and real-time tracking across RTP/FedNow, Same Day ACH, and international rails spanning 220+ countries.

The result: engineering teams ship faster, finance teams close books without manual reconciliation, and payees are paid on time, every time. With APIs driving 42% of revenue growth in leading financial institutions and API integrations in financial services increasing 54% in 2025, the right payment infrastructure isn’t just convenient—it’s a strategic competitive advantage.

Final Thoughts on API Payment Integration

Your payment API integration should make disbursements faster to ship and easier to maintain, not add another vendor relationship that creates more manual work. Routable gives you webhook events for every payment status change, idempotency to prevent duplicate transactions, and bi-directional ERP sync that keeps your books accurate without reconciliation spreadsheets. Start with our sandbox environment and see how quickly you can trigger your first programmatic payout.

FAQ

How do I choose the right API payment platform for my payout needs?

Start by evaluating your technical requirements: webhook support for real-time status updates, idempotency to prevent duplicate payments, and REST API quality. Then assess your operational needs like international coverage, instant payment rails (RTP/FedNow), and whether you need automated tax compliance (W-9/1099 collection). Finally, consider your finance team’s requirements for ERP integration and reconciliation workflows.

Which API payment platform works best for high-volume disbursements?

Routable is purpose-built for mass payout operations with 14 webhook events, idempotency keys, and support for instant payments through RTP/FedNow and Same Day ACH. Stripe Connect works well if you’re already using Stripe for payment acceptance, while Hyperwallet serves teams prioritizing rapid international deployment through PayPal’s ecosystem.

Can I integrate an API payment platform if my team also uses CSV uploads?

Yes, several platforms support both API and CSV workflows. Routable, Checkbook, and Trolley offer CSV upload options alongside their APIs, letting less technical team members process bulk payments while your developers use programmatic integration for automated disbursements triggered by your application logic.

What’s the difference between API-first payment platforms and traditional AP automation?

API-first platforms give your engineering team direct access to payment rails through code, letting you trigger disbursements based on your business logic (like paying a driver after delivery). Traditional AP tools focus on invoice processing with approval chains designed for finance teams managing supplier bills, not programmatic payouts to creators, gig workers, or sellers.

How long does API integration typically take for payment platforms?

Integration time varies by platform complexity and your requirements. Routable integrates in under 3 developer days for full implementation, while simpler platforms like Checkbook offer quick sandbox testing but lack compliance infrastructure.