You’re probably sending payments to program partners in Kenya, field researchers in Colombia, and local staff across Southeast Asia, which means you’re dealing with nonprofit international payment compliance whether you planned for it or not. The IRS requires W-8 forms before your first payout, OFAC screening before every disbursement, and 1042-S filings by March 15 regardless of whether you withheld taxes. Once you’re managing hundreds of monthly payments across multiple countries, manual processes create bottlenecks that delay disbursements and open compliance gaps you can’t afford during an audit.

TLDR:

- Collect W-8 forms before your first international payment to avoid defaulting to 30% backup withholding and year-end documentation scrambles when preparing Form 1042-S.

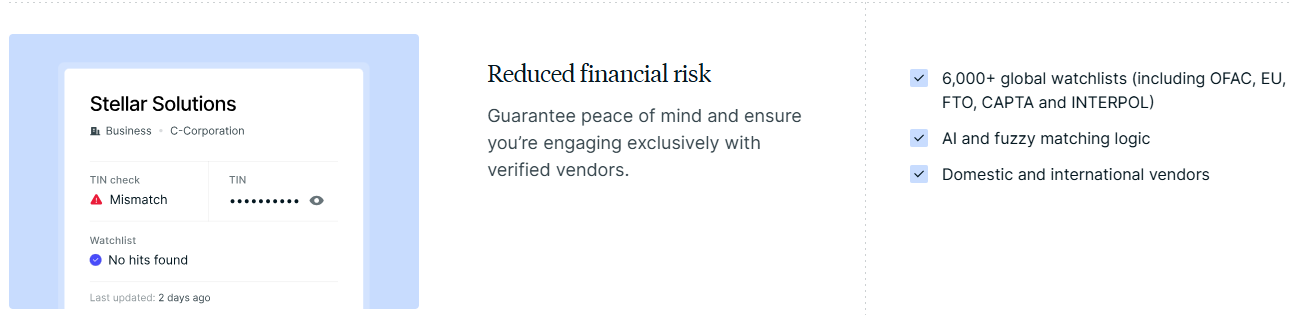

- Screen every international payee against OFAC sanctions lists at onboarding and before each payout, since lists update weekly and violations can result in account freezes and civil penalties.

- File Form 1042-S by March 15 for each reportable payment to foreign payees; organizations filing 10+ information returns annually must submit electronically through IRS FIRE.

- Automate tax form collection, sanctions screening, and treaty-based withholding calculations when disbursing to hundreds of field workers across multiple countries to prevent compliance gaps and audit risk.

- Choose payment rails based on destination and urgency: SWIFT reaches 200+ countries in 3-5 days at $15-$50 per transaction, while local rails clear faster (1-3 days) at lower cost in supported regions.

Why International Payment Compliance Matters for Nonprofits

When you send payments to international contributors, field researchers, or program partners, you’re subject to IRS, FinCEN, and OFAC oversight. Failed OFAC screening can freeze accounts. Failure to file Form 1042-S can result in IRS penalties and increased regulatory scrutiny. In addition, unresolved international tax compliance issues may negatively impact donor and grant-maker confidence during due diligence reviews.

Organizations disbursing to partners across 20+ countries need systems that automatically collect W-8 forms, screen sanctions lists, and generate year-end tax filings. Without that foundation, you’re one audit away from serious disruption.

Foreign Tax Form Requirements: W-8 Series Explained

When you pay a freelance journalist or a research partner outside your organization’s home jurisdiction, the IRS requires proof of their tax status before you can apply treaty benefits or determine withholding rates. That proof comes through the W-8 series.

W-8BEN covers foreign individuals. You’ll collect name, location, country of tax residence, and whether they qualify for reduced withholding under a tax treaty. Without it, you default to 30% backup withholding on reportable payments.

W-8BEN-E applies to foreign entities like NGOs, cooperatives, or consulting firms. This form requires entity classification, FATCA status, and beneficial owner details. Entity misclassification can trigger unnecessary withholding.

W-8EXP is for foreign governments, international organizations, and certain tax-exempt entities documenting exemption from withholding.

Automated collection during payee onboarding validates forms before the first payment, preventing withholding errors and year-end scrambles, much like compliant W-9 collection for domestic payees.

Form 1042-S Filing Obligations for Foreign Payees

Each reportable U.S.-source payment to a foreign payee requires a corresponding Form 1042-S by March 15, even if no tax was withheld. Missing the deadline can trigger per-form penalties that are adjusted annually and may start in the hundreds of dollars per return.

If you file 10 or more information returns in aggregate during the calendar year, Form 1042-S must be filed electronically through the IRS FIRE system. Many nonprofits cross this threshold once they start paying international researchers or field staff at scale.

The W-8 data you collect during onboarding flows directly into 1042-S preparation, similar to automating 1099s for domestic payees. Without accurate W-8s on file, you’re manually reconstructing payee details in February, risking mismatches that delay filing and trigger IRS notices.

OFAC Sanctions Screening for International Disbursements

Before sending international payments to gig workers or marketplace sellers, you must screen recipients against OFAC’s Specially Designated Nationals (SDN) list. Violations can result in civil fines and, in cases of willful misconduct, criminal penalties including fines up to $1 million and imprisonment of up to 20 years.

Screen at onboarding and before every payout. Sanctions lists change weekly, so previous clearance doesn’t guarantee current compliance.

High-volume payors sending hundreds of monthly disbursements need automated screening against global watchlists at both onboarding and payment execution, blocking prohibited transfers before funds leave your account.

Managing Default Withholding Tax Rates

The IRS applies a 30% withholding rate to foreign payees without proper documentation. Tax treaties with 65+ countries often reduce this to 0% to 15% when payees submit valid W-8 forms showing treaty residence and income type.

Your role is verifying the payee’s country matches an active treaty, the income qualifies under treaty terms, and the Taxpayer Identification Number follows that country’s format.

For high-volume disbursements to creators or contractors across treaty countries, automated systems cross-reference treaty tables at payment time, applying correct rates without manual review.

Fraud Prevention in International Payment Operations

International payments create unique fraud exposure. Ten percent of occupational fraud hits nonprofits, with median losses at $76,000. When disbursing to creators and field partners across countries, three vectors dominate: fake payee accounts, credential compromise, and payment rerouting.

Verify payee ownership at onboarding. Bank account validation confirms the person requesting payment actually controls the destination account. Without it, you’re sending funds based on self-reported details.

Separate payment creation from approval. The person initiating a $3,000 disbursement shouldn’t approve it. For amounts above your threshold, require dual authorization.

Real-time tracking catches fraud faster. When payees see expected dates and amounts in a self-service portal, they report discrepancies within hours instead of days. Automated alerts notify both you and the payee when payments clear or fail.

Cross-Border Payment Rails and Speed Considerations

SWIFT wires reach any country but take 3 to 5 business days and cost $15 to $50 per transaction. Correspondent banking networks add unpredictability, with each intermediary bank deducting fees that can reduce a $1,000 payment to $960.

Local rails bypass correspondent chains, clearing in 1 to 3 business days at lower cost, though coverage varies by country. PayPal works for smaller amounts when speed matters more than fees.

For organizations paying hundreds of creators or gig workers monthly, rail choice directly affects retention. When partners expect reliable arrival dates across 140+ currencies, you need systems that automatically route payments through the fastest, lowest-cost rail for each destination.

Building a Sanctions Compliance Program

OFAC guidance defines five core elements for sanctions compliance: management commitment, risk assessment, internal controls, testing, and training.

Management commitment requires board sponsorship and a compliance officer authorized to block disbursements when risks appear. Document screening procedures, escalation paths, and remediation steps.

Risk assessment maps payee locations. Organizations disbursing to creators across 40+ countries face different exposure than those in treaty nations. Higher-risk geographies require enhanced due diligence before onboarding.

Internal controls separate screening from payout execution. The person who screens a new contractor shouldn’t approve their first disbursement. Automated screening at onboarding and pre-payment reduces manual check failures under high volume.

Annual audits test control effectiveness. Sample recent international disbursements and verify each passed screening. Training keeps teams current when sanctions lists expand.

Automating Compliance for Mass Payouts

When you’re disbursing to hundreds of gig workers or program partners monthly, manual W-8 collection and sanctions screening create bottlenecks that delay payouts and open compliance gaps.

API-first payment infrastructure collects tax forms during payee onboarding, screens against multiple watchlists at both onboarding and payment execution, and calculates treaty-based withholding rates before funds move. CSV upload handles bulk disbursements when you’re not integrating directly.

This approach scales international operations without adding compliance headcount for every 100 new payees while maintaining audit-ready records.

How Routable Simplifies International Payment Compliance for Mission-Driven Organizations

Routable was built for organizations that disburse to hundreds of field workers, local partners, and program contributors across regions. White-label onboarding collects W-8 forms before the first payment, and automated screening checks 6,000+ watchlists at both onboarding and payout. API or CSV upload sends mass disbursements without invoice workflows.

Mongabay moved from their previous solution after chatbot support failed to resolve South Asia payment blockages. Our team worked directly via Slack to create custom payment paths when regional exchange rules shifted overnight. Sage Intacct sync kept their general ledger current across 36 currencies without manual reconciliation.

You maintain a lean team while scaling international disbursements to 220+ countries.

Final Thoughts on Scaling International Disbursements for Nonprofits

Building solid nonprofit international payment compliance prevents the bottlenecks that slow down your global work. Automated tax form collection and sanctions screening let you disburse to field researchers and program partners across dozens of countries without manual checks for every payment. You grow your international footprint while keeping compliance risk low and audit trails clean.

Schedule a demo to see how Routable handles W-8 collection, OFAC screening, and 1042-S preparation for organizations disbursing across 220+ countries.

FAQ

What happens if I pay a foreign contractor without collecting a W-8 form?

You default to 30% backup withholding on reportable payments, and you’ll face scrambles at year-end when preparing Form 1042-S. Collecting W-8 forms during onboarding prevents withholding errors and gives you the documentation needed for treaty-based rate reductions.

How often do I need to screen payees against OFAC sanctions lists?

Screen at onboarding and before every payout, since sanctions lists change weekly. Relying on previous clearance creates compliance gaps that can result in account freezes and civil penalties.

When is the deadline for Form 1042-S, and who needs to file electronically?

Form 1042-S is due by March 15 for the prior calendar year. If you file 10 or more information returns in aggregate during the year, you must submit electronically through the IRS FIRE system.

Can I use local payment rails instead of SWIFT for all international disbursements?

Local rails work for many countries and clear faster (1-3 business days) at lower cost, but coverage varies by destination. SWIFT reaches 200+ countries universally, making it the fallback when local rails aren’t available.

How do I know which tax treaty rate applies to a specific payment?

Your payment system should cross-reference the payee’s W-8 country against IRS treaty tables, verify the income type qualifies, and confirm the Taxpayer Identification Number format. Automated systems handle this lookup at payment time without manual review.