In 2026, global payouts are the infrastructure layer that determines whether your contractor network scales or stalls. Companies can distribute payouts to contractors, creators, affiliates, and gig workers across 220+ countries through a single platform, with local currency delivery, built-in compliance, and faster settlement. Managing payment rails, FX fees, tax documentation, sanctions screening, and recipient experience across dozens of regions demands purpose-built infrastructure. This guide covers how modern global payout systems work and what to look for in a scalable mass payments platform.

TLDR:

- Global payouts route funds to thousands of payees across 220+ countries using local rails, SWIFT, or real-time networks

- API-first infrastructure scales from 500 to 50,000 monthly payments without adding headcount

- Automated W-8/W-9 collection and 1042-S/1099-NEC output eliminate year-end filing backlogs at volume

- Payment speed shapes retention: platforms paying instantly keep more contractors than slower-paying competitors

- Purpose-built mass payout platforms handle programmatic disbursements via API or CSV, with white-label onboarding and real-time status tracking

What Are Global Payouts and Why They Matter in 2026

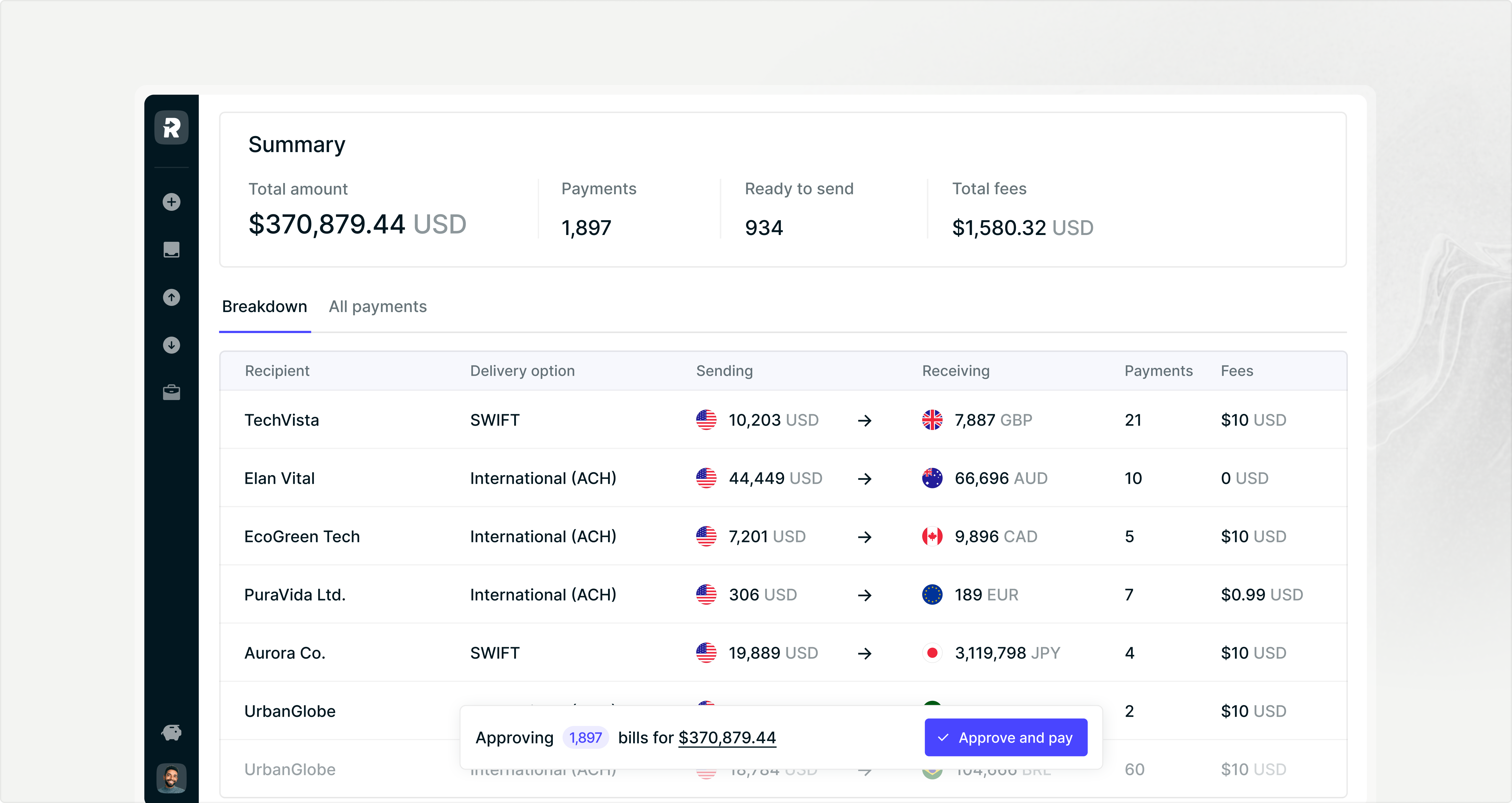

Global payouts are bulk disbursements sent simultaneously to payees across multiple countries, currencies, and payment rails. A single wire transfer moves money to one recipient. A global payout operation moves funds to thousands of creators, gig workers, or grant recipients in a single batch, across dozens of banking systems at once.

In 2026, that scale is the baseline. Platforms managing contractor networks across multiple countries cannot afford disbursement infrastructure that processes payments one at a time.

The stakes are direct: slow or failed payouts push contractors toward competing platforms that pay faster.

Payment Rails for International Mass Payments: SWIFT, Local Rails, and Real-Time Networks

Choosing the right payment rail for international mass payouts affects settlement speed, cost per transaction, and failure rates across your entire payee population.

Three main options dominate cross-border disbursements:

- SWIFT is the legacy default for international bank transfers. It reaches virtually every country, but fees run high and settlement typically takes three to five business days. At scale, that lag creates real cash flow exposure.

- Local payment rails — ACH equivalents, SEPA, UPI, Faster Payments — route disbursements through domestic networks in the destination country. That cuts costs and accelerates settlement to one to two business days, or same-day in supported corridors.

- Real-time payment networks are expanding across Asia-Pacific, Latin America, and Europe. Where infrastructure exists, settlement drops to minutes instead of days.

Rail selection is not a back-office detail. When you’re disbursing to thousands of creators, drivers, or grantees across multiple countries, the rail you choose directly shapes payee retention. Delayed settlements generate support tickets, erode trust, and push payees toward competitors who pay faster.

Most high-volume operators run a hybrid approach: local rails where available, SWIFT as the fallback for underserved corridors, and real-time networks where adoption warrants the integration cost.

How to Choose Payment Methods by Country and Region

Payment method availability varies by region. Choosing the wrong rail for a given country can mean failed disbursements, excessive FX fees, or payees who cannot receive funds at all.

Use this regional breakdown as a starting point:

API-First Payment Infrastructure vs. Manual Bank Portal Workflows

At low payment volumes, manual bank portal workflows are workable. Route thousands of payments across 220+ countries each month, and the choice between API-driven disbursements and manual portals stops being a preference and becomes a hard constraint.

Manual portals require finance team members to log in, upload files, approve batches, and monitor status one corridor at a time. At 5,000+ monthly payments across dozens of currencies, each manual touchpoint multiplies error risk and processing time in ways that don’t recover cleanly.

API-first infrastructure routes payments programmatically. Your system triggers disbursements directly — no human queuing at each step.

| Dimension | API-First Infrastructure | Manual Bank Portal |

|---|---|---|

| Payment initiation | Programmatic, triggered by your system | Manual login and file upload each cycle |

| Error handling | Automated retry logic and validation | Manual identification and resubmission |

| Status visibility | Real-time webhooks per transaction | Batch-level status, often delayed |

| Scalability | Handles volume spikes without added headcount | Throughput limited by team capacity |

| Compliance checks | Embedded at point of payment creation | Separate, often post-initiation |

The distinction matters most when volume spikes, corridors multiply, or your team can’t absorb another manual approval step without missing a pay cycle.

Tax Compliance for International Payouts: W-8, 1042-S, and Global Reporting

Every international payout carries a compliance obligation. Before funds leave your account, you need to know whether a payee is a U.S. person or foreign national, which determines the withholding rate applied and which tax form gets issued at year end.

Domestic contractors submit W-9s. International payees submit W-8 forms, which vary by entity type and treaty status. Getting this wrong at volume means incorrect withholding across hundreds of disbursements, followed by IRS penalties and manual remediation that compound every pay cycle.

At year end, domestic payees who crossed the reporting threshold receive 1099-NEC forms. Foreign payees receive 1042-S forms. Most high-volume operators hit a wall trying to run both populations through the same reporting workflow.

What Breaks at Scale

Three failure points repeat across global payout operations:

- W-8/W-9 collection left to payees without validation logic generates incomplete or expired forms that invalidate your compliance posture before a single payment goes out.

- Withholding rates applied without treaty verification default to the standard 30% rate, overpaying into escrow and creating refund requests that slow reconciliation.

- 1042-S/1099-NEC output generated from uncleaned data produces mismatch errors that trigger IRS notices, with penalties starting at $60 per form and scaling with volume.

Compliance automation that handles W-8/W-9 collection, treaty-aware withholding logic, and dual-form tax output is not a reporting convenience at scale. It is a prerequisite for running a cross-border payout operation without accumulating IRS penalties, incorrect withholding balances, and mismatch notices that multiply with every pay cycle.

Payment Speed as a Competitive Retention Tool for Gig Economy Platforms

Gig workers choose platforms based on how fast they get paid. A contractor paid within hours of completing a job is far less likely to accept a competing offer than one waiting three to five business days for a standard ACH settlement. At scale, that difference compounds across thousands of payees every pay cycle.

As of 2026, instant payout capability is no longer a differentiator. It is a baseline expectation. Many gig workers require same-day access to earnings to cover immediate expenses, and platforms relying on legacy batch-processing cycles face higher churn than those offering Real-Time Payments (RTP) or FedNow 24/7/365. When a worker can switch platforms in minutes, the payout experience is often the deciding factor.

Speed consistently shapes preference. Platforms that pay instantly retain more of their active contractor population because the payment itself becomes a reason to stay. The payout is a competitive tool, not a back-office transaction that trails the work.

Foreign Exchange Management and Multi-Currency Settlement

Currency volatility eats into contractor earnings before a payment even lands. When you’re disbursing to gig workers across multiple countries, even a 1-2% FX spread compounds into material losses at scale. Industry estimates put average cross-border remittance costs at around 6% per transaction. At that rate, a platform disbursing to 5,000 contractors monthly is absorbing serious FX drag before a single payee complaint comes in.

Most payout infrastructure treats currency conversion as an afterthought. Payees absorb unpredictable exchange rates, your finance team scrambles to resolve discrepancies, and failed disbursements spike whenever a local currency moves sharply.

Effective global payout operations require three things from your FX layer:

- Lock rates at the time of payment initiation, not settlement, so payees receive what they were promised regardless of intraday volatility.

- Pre-fund currency corridors in advance for high-volume routes to avoid settlement delays caused by liquidity gaps.

- Settle locally where possible to reduce conversion steps and the fees attached to each one. Fewer hops through correspondent banking networks mean lower costs and faster settlement for payees.

Without these controls, every international payment cycle carries embedded FX risk that grows proportionally with your payee count.

Sanctions Screening and Compliance Checks for Cross-Border Disbursements

Every cross-border payment carries sanctions exposure. Automated screening against global watchlists, including OFAC, EU, and FTO lists, must run at both payee onboarding and pre-payment execution. Onboarding checks alone are not enough.

Payee status changes. Geopolitical conditions shift.

Compliance holds must trigger at payment creation, not after funds are already in motion. With cross-border payment recovery rates under 5%, prevention is the only practical control once payments leave your system.

Scaling Mass Payments with Routable

Most payout infrastructure breaks at 1,000 monthly disbursements. Manual bank portals stall. Finance teams absorb manual work that compounds with every new payee corridor. Routable is built for the volume that comes after that threshold, handling 10,000+ monthly payments across 220+ countries and 140+ currencies without adding headcount or rebuilding workflows.

Two execution paths serve different team structures, and both are built to run at scale:

- API-first infrastructure lets engineering teams trigger disbursements programmatically the moment a payout event fires: a completed gig, approved grant, or finalized royalty split. Full production integration typically takes under three developer days. Idempotency key support prevents duplicate payments during network failures. Fourteen webhook events push real-time status back to your system, so payees stop asking your support team where their money is.

- CSV batch upload gives finance and ops teams a no-code path that processes thousands of cross-border payments in a single file. Fields auto-map to your general ledger. Duplicate detection runs before anything moves. No engineering dependency required to run a full international pay cycle.

White-label payee onboarding collects W-8 and W-9s and bank details through a custom-branded interface before the first payment goes out. That means tax compliance starts at onboarding, not at year end. Routable automatically cross-references W-8 country data against IRS treaty tables at payment execution to apply the correct withholding rate, with no manual review and no defaulting to 30% across your entire international payee population. At year end, the platform generates both 1042-S and 1099-NEC forms and automatically identifies which payees require which form.

Sanctions screening runs against 6,000+ watchlists at both payee onboarding and pre-payment execution, not at signup alone.

Final Thoughts on Mass Payment Operations That Don’t Break at Volume

Your global payout infrastructure isn’t a back-office detail when you’re paying thousands of contractors across multiple countries every month. It’s the mechanism that determines whether payees stay or switch to platforms that pay faster. Manual workflows that barely hold together today will collapse under the volume you’ll be running six months from now. If your current disbursement operation already requires workarounds to meet payment deadlines, see how Routable handles it without the manual intervention that’s slowing you down.

FAQ

Can I build a global payout operation without writing code?

Yes. CSV upload lets you process thousands of cross-border payments in a single batch without API integration. You map fields to your ledger, upload a formatted file, and Routable validates everything before funds move. As volume scales, you can switch to API-driven workflows without rebuilding your infrastructure.

Stripe global payouts vs. mass payment platforms for creator networks?

Stripe handles payment processing and one-off transfers but doesn’t automate W-8/W-9 collection, 1042-S/1099-NEC filing, or batch disbursements to thousands of payees across 220+ countries. Mass payment platforms are purpose-built for high-volume contractor networks that need programmatic disbursements, compliance automation, and white-label onboarding at scale.

What’s the fastest way to send payments to contractors across many countries?

Use local payment rails where available instead of defaulting to SWIFT. Local rails settle in one to two business days versus three to five for wire transfers, and they cut per-transaction costs from 3-5% to under 1%. Real-time payment networks accelerate settlement to minutes in supported corridors. Your payout platform should route automatically based on destination country without requiring manual rail selection.

How do I handle tax compliance when paying international contractors?

Collect W-8 forms from international payees and W-9s from domestic contractors during onboarding, before the first payment. At year end, issue 1042-S forms to foreign payees and 1099-NEC forms to domestic contractors who crossed the reporting threshold. Automated systems match treaty rates, apply correct withholding, and generate both form types without manual sorting.