Instant payments let platforms, marketplaces, and businesses send funds to users in minutes instead of days, often through debit card rails or real-time banking networks that operate 24/7. What started as a premium fintech feature is now an expectation across industries like gig work, creator platforms, ecommerce, and contractor marketplaces, where users want immediate access to earnings. For businesses, instant payments can improve trust and payee satisfaction, but they also introduce new challenges around fraud prevention, compliance, liquidity, and transaction costs. In this guide, we’ll explain how instant payments work, the infrastructure behind them, and when they make sense for your platform or product.

TLDR:

- Instant payments move funds to a payee’s bank account or debit card within minutes, bypassing standard ACH clearing windows that take one to five business days.

- The fastest rails are RTP and push-to-debit card networks; same-day ACH is a lower-cost middle ground that settles within hours instead of days.

- Instant payments carry a higher per-transaction cost, but for platforms disbursing at volume, the retention gains from faster payouts often offset the incremental fee. The math depends on your payee mix and how frequently you disburse.

- Use instant payments for gig workers, creators, and on-demand platforms where payment speed directly drives retention. Use scheduled batch disbursements for fixed-cycle payments like monthly royalties or recurring contractor runs.

- At scale, the routing decision between same-day ACH and RTP should be programmatic, based on urgency, payee type, and cost tolerance, not a manual call made each payment cycle.

What Are Instant Payments

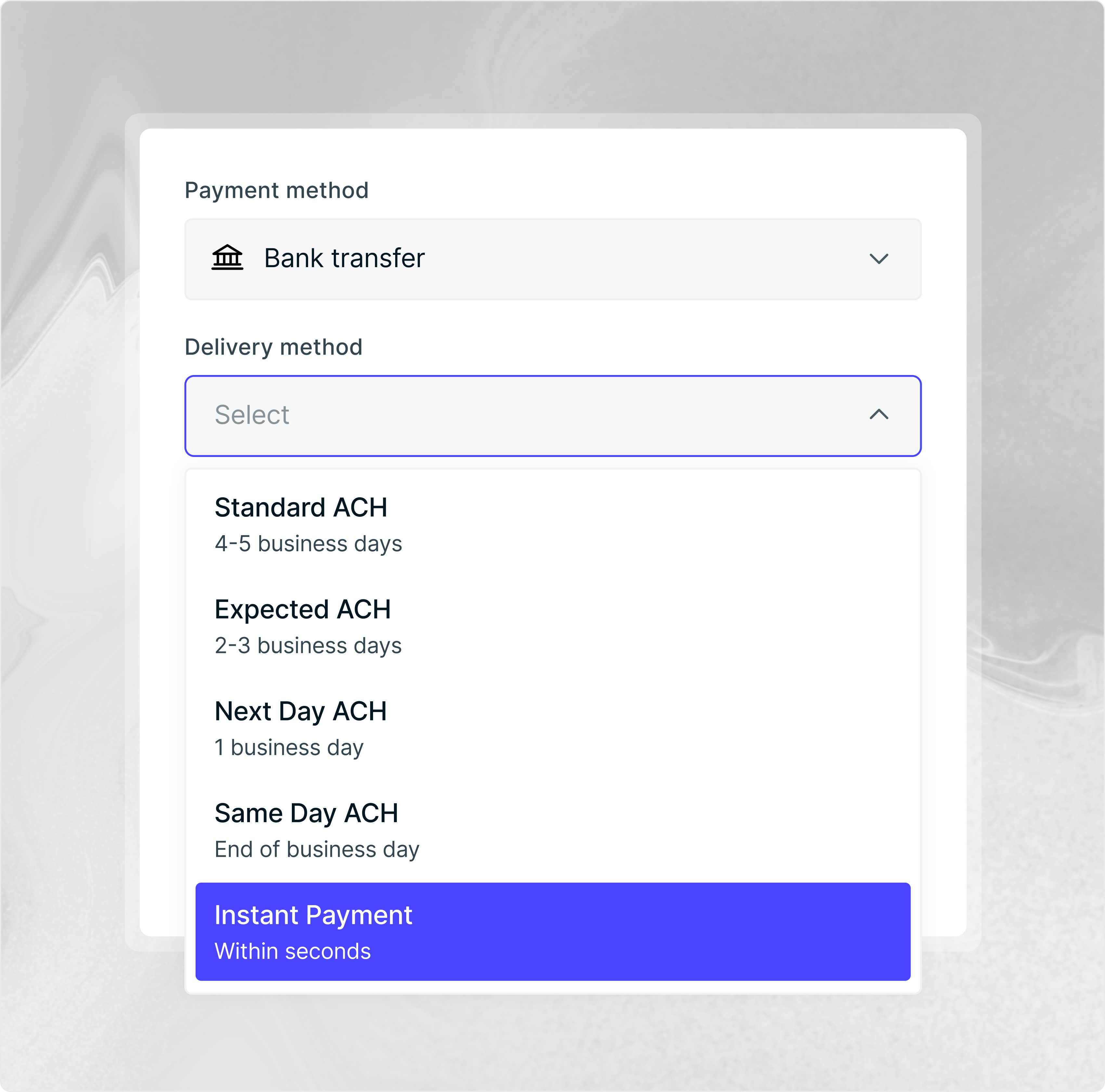

Instant payments move money from a payment source to a payee’s bank account or debit card within minutes, instead of the one to five business days standard ACH transfers typically require.

For platforms managing high-volume disbursements to creators, drivers, or gig workers, speed is a retention variable. The market reflects this shift: real-time payment transaction volumes in the US are projected to reach 8 billion in 2026 and nearly 13.9 billion by 2028, representing a compound annual growth rate of more than 30%. Payees who wait days for earnings are payees actively comparing your platform to a faster-paying competitor.

The core mechanics are straightforward: Instant payments bypass standard clearing windows by routing funds through real-time rails like RTP or card networks, settling in seconds to minutes instead of batching overnight.

How Instant Payments Work Across Payment Rails

Instant payments move across several distinct rails, each with different speed profiles, fee structures, and eligibility requirements.

Real-Time Payments (RTP) and FedNow

Real-Time Payments (RTP) and FedNow are the two primary instant payment rails in the U.S., both pushing funds directly to eligible bank accounts and typically settling in seconds. RTP is operated by The Clearing House; FedNow is the Federal Reserve’s instant payment service, now in its third year of operation and continuing to expand participating bank coverage. Both operate 24/7/365, including weekends and holidays. Coverage depends on whether the receiving bank participates in either network.

Instant ACH / Same-Day ACH

Some providers offer Same-Day ACH, which settles faster than standard ACH transfers. While traditional ACH can take one to three business days, Same-Day ACH often settles within hours during banking windows. It is not truly instant, but it provides broader bank coverage for accounts that do not support RTP or FedNow.

Debit Card Payments (Push-to-Card)

Funds reach a payee’s Visa or Mastercard debit card within minutes through card networks. This is the most accessible path for gig workers and creators who want immediate access to earnings without waiting on bank processing.

Instant Payment Speed Expectations in the Gig Economy

Speed consistently shapes preference. 81% of gig workers say they’d choose one platform over another based on instant pay capabilities, making payment speed a direct competitive differentiator and supporting the higher transaction fees as a retention investment.

Gig platforms paying drivers, creators, and independent contractors are feeling this most acutely. Workers compare payout speed across platforms the same way they compare rates. A platform that settles earnings weekly via standard ACH is competing against one offering same-day disbursements, and the gap shows up in retention numbers.

Same-day pay is no longer a nice-to-have. It’s the baseline workers expect, and platforms that can’t deliver it aren’t offering a slower benefit — they’re failing a requirement.

When to Use Instant Payments vs. Scheduled Disbursements

The decision hinges on whether payment timing changes payee behavior: whether a faster payout keeps a gig worker, creator, or driver on your platform instead of switching to a competitor that pays sooner.

When payees have competing options and can switch in a day, instant payments are a retention lever. When payment relationships are contractual and cycles are predictable, scheduled batch disbursements cost less and run leaner. Over-building instant infrastructure for payees on fixed schedules erodes margin. Let payee churn signals, not assumptions, tell you where speed actually moves the needle.

Cost Structure and Fee Comparison Across Instant Payment Methods

Instant payments cost more than standard transfers, and the gap widens depending on the method and provider.

Here is how the most common methods compare:

Faster methods do carry a higher per-transaction cost. However, improved payee retention and reduced churn often offset the incremental fees when you are disbursing at volume to gig workers, creators, or drivers whose platform loyalty tracks directly to payment speed.

Instant Payments for International Contractors and Cross-Border Disbursements

Cross-border instant payments introduce a layer of complexity that domestic disbursements don’t. Currency conversion, local banking rails, and regional compliance requirements all affect whether a payment reaches an international contractor quickly or gets stuck in a multi-day clearing queue.

Most instant payment infrastructure is built around U.S. debit card networks and domestic ACH. That means your international contractors, gig workers, and creators are often excluded from the same-day settlement options you offer domestically.

A few realities worth knowing:

- Coverage varies by country. Many instant payment providers support real-time settlement in the U.S. and UK, but drop to standard ACH or SWIFT timelines everywhere else.

- FX fees compound at scale. A 1-3% conversion fee applied across thousands of monthly cross-border disbursements adds up to material cost exposure fast.

- Local rail availability determines speed. In markets without real-time payment infrastructure, “instant” often means next-day at best.

If your contractor network spans multiple countries, assessing instant payment providers on their international rail coverage is as important as their domestic speed.

How Mass Payment Infrastructure Handles Instant Disbursements at Scale

Instant payments work well for individual transactions, but high-volume payment operations require infrastructure built to handle scale without breaking.

When you’re disbursing earnings to thousands of creators, drivers, or gig workers in a single cycle, the bottleneck is rarely the payment rail itself. It’s the orchestration layer sitting above it: payee onboarding, eligibility verification, routing logic, and reconciliation running in parallel across every transaction.

Purpose-built mass payment infrastructure handles this by separating disbursement logic from payment execution. Batch scheduling, programmatic routing, and automated payee validation run independently of whether the underlying transfer settles in seconds or days.

- Payee eligibility checks run at onboarding, not at disbursement, so instant payment requests don’t stall on verification.

- Routing logic selects the fastest available rail per payee based on bank support, geography, and account type.

- Reconciliation updates automatically regardless of settlement timing, keeping your books clean without manual intervention.

At scale, this architecture matters more than payment speed alone.

Why Routable Supports Same Day ACH and Real-Time Payments for High-Volume Platforms

Routable is built for operators running high-volume payment cycles where speed and reliability aren’t preferences — they’re requirements.

When you’re disbursing earnings to thousands of creators, drivers, or gig workers on a weekly or daily cycle, standard ACH settlement windows create real execution risk. Payees who don’t get paid on time don’t wait. They move to platforms that pay faster.

Same Day ACH and real-time payment rails give your disbursement infrastructure the speed those payees expect. Routable supports both, so you’re not forced to choose between cost and responsiveness based on what your rails can handle.

- Same Day ACH settles within hours instead of the typical multi-day window, covering the majority of high-volume domestic payment use cases without the per-transaction cost of card-based instant methods.

- Real-time payments reach payees’ accounts in seconds, which matters most for time-sensitive disbursements where settlement delays directly affect payee behavior and retention.

At scale, the difference between these two rails is a routing decision your infrastructure should make programmatically, based on urgency, payee type, and cost tolerance, not a manual call your team makes per payment cycle.

Routable’s API-first architecture handles that routing logic at volume, processing thousands of disbursements per cycle without adding headcount or introducing manual bottlenecks.

Final Thoughts on Instant Payment Speed and Scale

Your payment infrastructure is product. When it pays slower than competing platforms, you’re losing speed and you’re losing payees to services that handle instant payments without delays or manual bottlenecks. Routable routes disbursements across same-day ACH and RTP rails automatically, so your system scales without breaking when volume doubles. See how it works when you’re processing thousands of payments per cycle and can’t afford to wait on settlement windows your competitors already eliminated.

Frequently Asked Questions About Instant Payments

What is the difference between instant payments and same-day ACH?

Instant payments, delivered via Real-Time Payments (RTP) or FedNow rails, settle in seconds, 24/7/365, including weekends and holidays. Same-day ACH settles within hours but only during banking windows on business days. Same-day ACH costs less per transaction and reaches more bank accounts; RTP is faster but depends on whether the receiving bank participates in the network.

How much do instant payments cost compared to standard ACH?

Standard ACH is low-cost or free. Same-day ACH typically runs $0.25 to $1.00 per transaction. RTP and FedNow often use flat-fee pricing under $1.00 per transaction. Push-to-debit methods like Visa Direct and Mastercard Move run roughly 0.5% to 1.5% per transaction. For gig platforms and creator marketplaces paying at volume, the incremental cost per transaction is typically offset by reduced payee churn.

Which payment rail should I use for gig worker payouts?

For time-sensitive payouts where settlement speed directly affects whether a worker stays on your platform, RTP or FedNow delivers funds in seconds and operates around the clock. Same-day ACH is a solid lower-cost alternative for high-volume domestic disbursements where same-business-day settlement is sufficient. Push-to-debit works well for payees who want earnings sent directly to a debit card. The right routing decision depends on urgency, bank coverage, and your per-transaction cost tolerance.

Can instant payments be used for international contractors?

Most instant payment infrastructure, including RTP, FedNow, and push-to-debit card networks, is built around U.S. domestic rails. International contractors are typically excluded from same-day settlement options available domestically. Cross-border disbursements often default to SWIFT or local rails, which can take one to five business days depending on the destination country. If your contractor network spans multiple countries, assess providers on their international rail coverage alongside their domestic instant payment capabilities.

When should I use scheduled batch disbursements instead of instant payments?

Scheduled batch disbursements make more sense when payment relationships are contractual, cycles are predictable, and payees aren’t comparing your payout speed against a competitor’s. Monthly royalty distributions, recurring contractor runs on fixed schedules, and payroll for workers on set pay cycles are all cases where batch processing costs less and runs leaner. Instant payment infrastructure is best reserved for payee populations where payment speed is a retention variable: gig workers, on-demand creators, and independent contractors who can switch platforms in a day.