Building two-sided marketplace companies means managing a paradox: buyers need sellers, sellers need buyers, and neither will show up first. Most operators focus on subsidizing one side to bootstrap growth, but there’s a simpler lever nobody talks about: how you move money to providers. When creators can track their earnings in real time and cash out instantly on your platform while competitors make them wait for monthly checks, you’ve just solved your supply problem without spending a dollar on acquisition. We’ll break down how these platforms work and why payment infrastructure matters more than most founders realize.

TLDR:

- Two-sided marketplaces connect buyers and sellers without owning inventory or hiring suppliers.

- Network effects drive growth: more supply attracts demand, which attracts more supply.

- Payment speed determines which marketplaces win talent; 46% of U.S. workers now expect instant payouts.

- API-first systems let you trigger thousands of programmatic disbursements without manual intervention.

- Routable handles mass payouts with same-day settlement, automated tax compliance, and 220+ country coverage.

What Is a Two-Sided Marketplace?

A two-sided marketplace connects two distinct user groups who each deliver value to the other. One side supplies a good or service (sellers, creators, drivers), while the other demands it (buyers, riders, customers). The marketplace doesn’t own inventory or hire suppliers but creates the infrastructure for direct transactions.

Examples include Uber connecting riders and drivers, Airbnb linking travelers and hosts, or Etsy bringing together shoppers and artisans. The marketplace earns revenue from each exchange through transaction fees, commissions, or subscriptions. Value flows both ways, and growth depends on active participation from both sides.

How Two-Sided Marketplaces Work

The marketplace matches buyers with sellers and handles transaction infrastructure. When a buyer requests a product or service, the system routes demand to qualified suppliers. After the transaction, the marketplace collects payment, deducts its fee, and disburses funds to the seller.

Three layers power this flow: onboarding that validates both sides, transaction coordination that matches requests with fulfillment, and disbursement infrastructure that moves money to payees. The third layer breaks first. When you’re processing 500 payouts manually through a bank portal, you’re one sick day away from missing a pay cycle. When drivers can’t track payout status or don’t know which bank account will receive funds, your support queue fills with payment questions instead of product feedback. When a creator sees “processing” for five days while a competitor pays instantly, they move their content elsewhere.

Disbursement infrastructure determines which marketplaces retain supply. Operators managing hundreds of sellers learn that payout speed, transparency, and reliability matter more than transaction fees or feature lists. A marketplace that pays creators same-day while competitors batch weekly payouts solves retention without spending a dollar on acquisition incentives.

Two-Sided Marketplace Examples Across High-Growth Verticals

Gig Economy

Uber and DoorDash pay drivers daily or instantly to compete for labor. When drivers can cash out in real time on one app but wait three days on another, they shift hours to the faster option.

Creator Economy

Substack disburses subscription revenue to writers. White-labeled onboarding and transparent payout timelines keep creators engaged.

Logistics and Delivery

Veho and GoShare manage fleets of independent couriers who expect same-day or next-day settlement. Payment speed directly impacts driver retention, especially when competitors offer instant payout options.

Resale and Peer-to-Peer Commerce

Garmentory connects boutique sellers with shoppers. Poshmark pays sellers after buyer confirmation. Seasonal surges create payout backlogs if disbursement infrastructure can’t scale.

Network Effects: The Growth Engine of Two-Sided Markets

Cross-side network effects occur when growth on one side attracts more users on the other. More riders on Uber pull in more drivers; more drivers lower wait times and attract more riders. Online marketplaces account for 63.5% of all online sales in 2025. Understanding mass payouts is critical for scaling these platforms.

Payment infrastructure sits at the center of this loop. If a gig worker waits five days for payout while a rival offers same-day settlement, they’ll shift their labor elsewhere. Delayed disbursements erode supply-side participation, weakening demand-side engagement.

A marketplace that pays creators instantly retains them better and attracts new supply, which improves selection for buyers, drives more transactions, and funds faster payouts.

Mass Payout Infrastructure for High-Volume Marketplaces

Marketplaces processing 10,000+ monthly disbursements need infrastructure that handles volume without manual intervention. API-first systems let operators programmatically create payouts tied to transaction events like completed deliveries or commission settlements. CSV uploads give ops teams batch control when payment logic lives in internal databases or spreadsheets.

Over 70% of independent workers said they would leave their current freelancer marketplaces for better payment experiences. That makes disbursement infrastructure a retention lever. Real-time status tracking surfaces failed payments before providers notice, and flexible payment rails let marketplaces offer ACH, instant transfers, or PayPal based on payee preference.

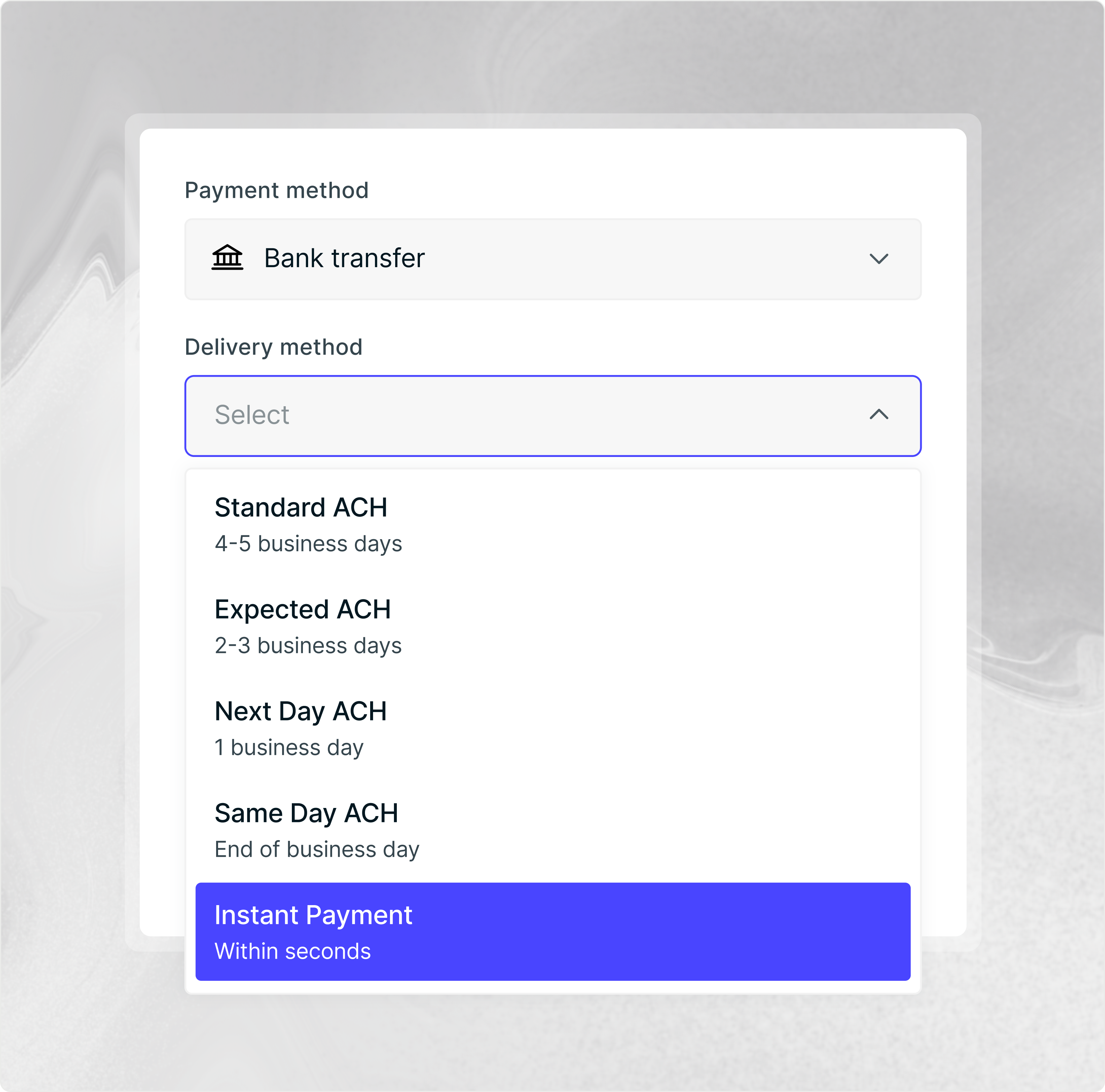

Payment Speed as a Competitive Advantage

Payout speed has shifted from a back-office detail to a product feature that determines which marketplaces win supply. 46% of U.S. workers now receive payouts instantly most of the time, resetting baseline expectations for high-volume payout solutions. A driver choosing between two delivery apps will default to the one that clears funds by evening instead of waiting three business days.

91% of gig workers want more frequent payouts than the traditional two-week payroll cycle. Same-day ACH or RTP becomes the tiebreaker when every rideshare app offers similar per-trip earnings.

API-First Disbursement Systems for Programmatic Control

Manual bank portals force operators to initiate payouts individually, creating bottlenecks when monthly disbursements exceed a few hundred. API-driven systems let marketplaces programmatically trigger payouts the moment a transaction completes or milestone clears.

External ID mapping ties every payout to internal ride IDs, order numbers, or commission records. When a driver disputes payment timing, ops teams instantly trace the disbursement to the originating event without manually checking spreadsheets. Idempotency keys prevent duplicate payments during network failures or retries.

Operators start with CSV uploads for batch control, then migrate to full API integration as volume scales.

Payee Experience: Onboarding, Transparency, and Payout Choice

White-labeled onboarding removes confusion. When drivers or creators see the marketplace’s branding throughout setup instead of a third-party processor’s name, they trust the experience and complete enrollment faster.

Bank account validation during onboarding reduces failed payments caused by mistyped routing numbers. Self-service detail updates let payees fix information without contacting support. Real-time status visibility answers “where’s my money?” before it becomes a ticket.

Payment method choice matters. Some creators prefer ACH for lower fees. Gig workers may choose instant transfers for same-day access.

Tax Compliance and 1099 Management at Scale

Mass payouts to thousands of creators, drivers, or sellers generate tax obligations that multiply with every new payee. Anyone earning above the IRS threshold needs proper documentation, and manual collection delays onboarding.

Automated W-9 capture during signup pulls taxpayer details before the first disbursement. Real-time TIN validation checks names against IRS records, catching mismatches before they trigger B-notices. W-8 forms handle international payees and withholding requirements.

Year-end 1099-NEC and 1099-MISC filing grows unmanageable without automation. Systems that track earnings year-round generate forms automatically, while 1042-S preparation covers foreign recipients.

How Routable Powers Mass Payouts for Two-Sided Marketplaces

Routable gives marketplace operators disbursement infrastructure that scales with transaction volume. Our REST API integrates quickly, letting you trigger payouts programmatically the moment a delivery completes or commission settles.

You control which rails fit your economics: Same Day ACH, Next Day ACH, Real-Time Payments, or international transfers to 220+ countries. White-labeled onboarding collects bank details and tax forms automatically, with year-end 1099 and 1042-S filing handled without manual intervention.

14 webhook events notify your system when payments clear or fail. External ID mapping ties every disbursement back to internal transaction records.

Final Thoughts on Scaling Two-Sided Marketplace Payouts

Every successful two-sided marketplace solves the same core problem: getting both sides to participate consistently. Fast, reliable payouts keep your supply side engaged, which improves selection for buyers and drives more transactions. Routable handles disbursement infrastructure so you can focus on growth instead of manual payment operations. Your marketplace wins when providers choose you over competitors, and same-day settlement makes that choice obvious.

FAQ

How do two-sided marketplaces make money?

Two-sided marketplaces collect transaction fees, commissions, or subscriptions from exchanges between buyers and sellers. The marketplace doesn’t own inventory but takes a percentage when value moves between both sides, like Uber charging riders and deducting a fee before paying drivers.

What’s the main difference between one-sided and two-sided marketplaces?

One-sided marketplaces control inventory and sell directly to customers, like Amazon Retail. Two-sided marketplaces connect independent suppliers with buyers without owning products, splitting payment between the operator’s fee and disbursements to sellers or service providers.

Why does payout speed matter for marketplace retention?

Over 70% of independent workers would leave their current platform for better payment experiences. When drivers or creators can get paid instantly on one app but wait three days on another, they shift their labor to the faster option, making disbursement speed a direct retention lever.

How do API-first systems improve mass payout operations?

API-driven disbursement lets you programmatically trigger payouts the moment a transaction completes, eliminating manual bank portals. External ID mapping ties every payment to internal records, while idempotency keys prevent duplicate payments during network failures or retries.

When should a marketplace automate tax compliance?

Automate tax collection once you’re disbursing to dozens of payees earning $600+ annually. Manual W-9 gathering delays onboarding and creates year-end filing bottlenecks. Automated systems capture taxpayer details during signup and generate 1099-NEC, 1099-MISC, or 1042-S forms without manual work.