When you’re disbursing to thousands of creators or gig workers each month, Stripe Connect’s per-transaction and per-payout fees compound fast. Your payout amounts live in your own database, so why pay for connected account infrastructure you don’t need? If you want Stripe alternatives that give you Same Day ACH, instant payments, proper webhook coverage, and idempotency protection, there are better options. Let’s break down what actually works for high-volume programmatic payouts.

TLDR:

- Stripe Connect forces re-onboarding of all payees during Standard-to-Express migration

- Routable offers Same Day ACH and instant RTP/FedNow rails for faster payouts vs Stripe

- Stripes’s per-transaction and per-payout fees compound fast at scale—alternatives built for mass disbursements offer better economics

- Routable handles 10,000+ monthly payouts with bi-directional ERP sync at 99.8% accuracy

- Routable is an API-first payment infrastructure for marketplaces and gig platforms

What Is Stripe Connect and How Does It Work?

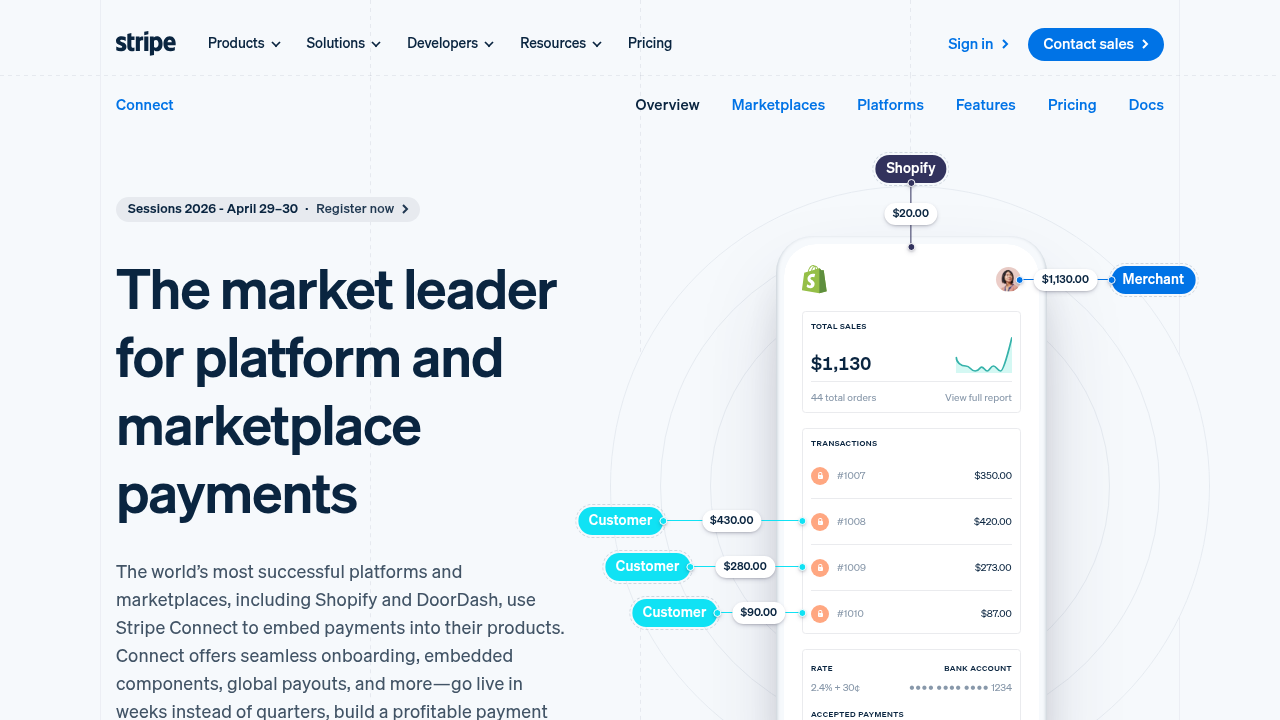

Stripe Connect is a payments platform designed for marketplaces, gig economy apps, and other multi-sided businesses that need to accept payments and route funds to third parties. Instead of building payout, compliance, and onboarding infrastructure in-house, engineering teams integrate Stripe Connect to automate payment collection, split payments, seller onboarding, and disbursements to creators, drivers, or service providers.

The product is built around a connected account model, where each seller or provider is linked to the platform’s Stripe account. Platforms can choose between Standard, Express, and Custom accounts depending on how much control they want over the user experience and compliance responsibilities. Stripe handles core functions like identity verification, tax reporting support (including U.S. 1099 forms), payout scheduling, and multi-currency payments across dozens of countries, while offering flexibility in how much of the Stripe dashboard and branding is exposed to payees.

Pricing combines Stripe’s standard payment processing fees with additional Connect-specific charges that vary by account type and features used, such as per-payout fees, instant payout fees, FX conversion, and local payment method costs. For high-volume operations disbursing thousands of monthly payouts to drivers, creators, or gig workers, these incremental fees can add up quickly, driving many companies to evaluate other options.

Why Consider Stripe Connect Alternatives?

Stripe Connect works well for marketplaces and platforms that want tightly integrated payment acceptance and payee onboarding within a unified Stripe ecosystem. The connected account model, built-in KYC flows, and automated U.S. 1099 reporting reduce the need to build compliance infrastructure from scratch.

Organizations sometimes evaluate alternatives when their payout logic is fully decoupled from buyer payment flows or when they need highly customized ledger control outside the connected account paradigm. Because Connect is fundamentally account-centric, it may introduce additional architectural considerations for companies that simply need to execute high-volume disbursements calculated in their own internal systems.

For platforms considering a migration from Stripe Connect Standard to Express accounts, the migration process is complex and requires re-onboarding every single payee through new verification flows. For platforms with thousands of active creators, drivers, or sellers, this creates months of operational work and introduces significant churn risk. Payees who already completed KYC must verify their information again, leading to confusion, support tickets, and potential attrition to competitors with smoother payout experiences.

Stripe offers multiple payout methods, instant payout options, and global coverage, but costs can increase with scale due to layered processing, payout, FX, and optional feature fees. Companies with complex ERP synchronization requirements, specialized treasury workflows, or highly customized developer tooling needs may benchmark Connect against providers focused specifically on programmable disbursements.

Best Stripe Connect Alternatives in February 2026

Routable (Best Overall Alternative)

Routable is an API-first payment infrastructure provider built for high-volume mass payouts. We serve marketplaces, gig economy apps, logistics networks, and creator businesses that need programmatic disbursements without forcing payments through invoice approval workflows designed for traditional finance teams.

Our REST API includes 14 webhook events, idempotency keys, and sub-3 developer day integration time. You get Same Day ACH, RTP/FedNow instant payments, checks, wires, and international coverage across 220+ countries. Compliance automation includes W-8 and W-9 collection, 1042-S and 1099 filing, TIN validation, and over 6,000 watchlist checks, all running without manual intervention. Bi-directional ERP synchronization with NetSuite, Intacct, QuickBooks, and Xero maintains 99.8% accuracy.

Routable works for engineering teams that need to trigger payouts programmatically based on their own business logic rather than manage connected seller accounts. Companies looking to avoid the Stripe Standard to Express migration disruption find we handle the transition without re-onboarding every payee.

You get payout infrastructure without becoming a payments company. Faster payment rails, stronger compliance automation, better ERP connectivity, and developer tooling purpose-built for disbursements instead of treating payouts as an afterthought to buyer checkout flows.

Hyperwallet

Hyperwallet is PayPal’s mass payout platform designed for global creator, freelancer, and contractor disbursements. It offers pre-built, hosted payee experiences and broad international reach across multiple payout methods, including PayPal balances, cards, and bank transfers. Companies already embedded in the PayPal ecosystem or prioritizing rapid deployment over deep customization often find Hyperwallet a strong fit.

The payee experience primarily lives within the PayPal and Hyperwallet environment, which limits branding control and flexibility compared to API-first payout infrastructure. While the platform supports batch processing and API-driven payouts, it provides less control over internal ledger synchronization, reconciliation workflows, and nuanced compliance exception handling. Developer tooling is more opinionated, making it less suitable for teams that require highly customized payout logic tightly integrated with internal systems.

Checkbook

Checkbook is a push-payments provider offering ACH, virtual card, and digital check disbursements through a lightweight API, with sandbox and Postman testing support. Teams that need basic payment execution with minimal vendor management requirements can deploy quickly and avoid the complexity of full marketplace or payout infrastructure.

The platform emphasizes simplicity over depth. Vendor management features such as automated tax form collection, compliance screening, and KYC workflows are limited and typically handled outside the system. Operational tooling for bulk actions, exception handling, reconciliation, and advanced reporting is relatively minimal. While the API supports safeguards against duplicate payments, idempotency and retry handling are less robust than in payout platforms built for high-volume, fault-tolerant workflows. Checkbook also lacks native ERP integrations, requiring teams to build custom reconciliation processes for accounting and month-end close.

Trolley

Trolley is a global payout platform designed for internet-economy businesses with a strong emphasis on tax compliance. The product supports W-8 and W-9 collection, U.S. tax form filing, and international payouts across a broad set of countries, making it a common choice for companies with globally distributed payees and complex tax reporting needs.

The platform focuses primarily on payouts and tax workflows rather than end-to-end operational controls. Workflow customization and approval hierarchies are more limited than in full treasury or accounts-payable systems, and ERP integrations tend to rely on basic connectivity or exports rather than deep, bi-directional synchronization. While the API supports safeguards against duplicate payments using external identifiers, idempotency and retry handling are less robust than in payout infrastructure built for high-volume, fault-tolerant execution. Commercial terms and minimum volumes can also make Trolley a better fit for mid- to high-scale programs rather than smaller payout use cases.

Tipalti

Tipalti is a global mass payout solution used by marketplaces and gig businesses to manage multi-currency disbursements at scale. The platform handles contractor onboarding, tax form collection, and managed compliance workflows, while supporting a wide range of payment methods across international jurisdictions. Teams that prioritize turnkey global coverage and outsourced compliance often value Tipalti’s breadth and operational depth.

Compared to API-first payout providers, Tipalti typically involves higher upfront costs and longer implementation timelines, reflecting its focus on finance-led workflows and managed services. The interface and feature set are optimized for accounts payable and operations teams rather than developers building custom payout logic. While APIs are available, they offer less flexibility for fully programmatic, event-driven payout triggering than platforms designed primarily for engineering-centric disbursement use cases.

Feature Comparison: Stripe Connect vs Top Alternatives

The table below compares API capabilities, payment rails, compliance features, and operational tooling across six payment infrastructure providers. If you’re evaluating which solution fits your mass payout needs, this breakdown shows where each offers distinct strengths.

Routable offers the most complete solution because it combines fast, developer-friendly API integration with instant payment rails, broad international coverage, robust ERP sync, full approval workflow support, and built-in idempotency protection—covering both engineering and operational needs that other platforms only address partially.

Why Routable Is the Best Stripe Connect Alternative

The API architecture treats disbursements as first-class infrastructure. You calculate payout amounts in your own system, trigger payments via REST endpoint, and receive webhook notifications as funds move. No connected account overhead, no seller dashboard management, no building around checkout flow constraints. Global payment volumes reached $2.5 trillion in 2025, and companies processing high transaction counts need infrastructure that scales without per-transaction pricing models that compound at volume.

Unlike Stripe Connect, where migrating from Standard to Express accounts requires re-onboarding every payee, Routable lets platforms move existing payment data seamlessly, preserving your payee base. For marketplaces, gig networks, and creator businesses with thousands of drivers, sellers, or creators, this avoids months of operational work and reduces churn risk.

Built for engineering teams who view payments as core product infrastructure rather than back-office finance, Routable offers Same Day ACH and instant RTP/FedNow rails to improve payee retention, compliance automation to eliminate operational bottlenecks, and ERP connectivity that keeps finance teams aligned without manual CSV exports.

For businesses that require programmatic mass payouts, flexible payment rails, strong compliance tooling, and a developer experience purpose-built for disbursements rather than checkout, Routable provides capabilities that Stripe Connect leaves out.

Final Thoughts on Evaluating Stripe Connect Alternatives

Your marketplace payments setup should match your actual workflow, not force you into account models designed for different use cases. Companies with high payout volumes need infrastructure that scales without compounding per-transaction fees or migration headaches. If you calculate payout logic in your own system and just need reliable execution with fast rails and tax compliance, alternatives built for programmatic disbursements make more sense.

Talk to our team about how Routable handles mass payouts for gig networks and creator businesses.

FAQ

When should you consider switching from Stripe Connect?

You should consider alternatives if you’re triggering payouts based on your own business logic rather than managing connected seller accounts, if you need Same Day ACH or instant payment rails to improve payee retention, or if Stripe is forcing your Standard account migration and re-onboarding thousands of payees creates operational risk.

What features should you prioritize when comparing mass payout alternatives?

Prioritize idempotency key support to prevent duplicate payments during network issues, faster payment rails like RTP/FedNow for competitive payee experience, automated tax compliance with W-9/1099 collection, and bi-directional ERP sync if your finance team needs automated reconciliation without manual CSV exports.

How does API integration complexity differ across payout providers?

Stripe Connect requires building around connected account models and checkout flow constraints with substantial developer effort. Routable delivers REST API integration in under 3 developer days with 14 webhook events and idempotency protection, while providers like Hyperwallet offer drop-in UI components that sacrifice control for deployment speed.

Can I migrate from Stripe Connect without re-onboarding my payees?

Yes—Routable handles the transition by migrating your existing payment data without requiring payees to complete new KYC flows. This prevents the operational disruption and churn risk that comes from asking thousands of drivers, creators, or sellers to re-verify their information through a new system.

What payment rails matter most for payee retention in gig and marketplace businesses?

Same Day ACH and instant payment options like RTP/FedNow directly impact whether payees stay on your network versus competitors offering faster disbursements. Standard ACH taking 4-5 business days creates retention issues when gig workers and creators expect next-day or same-day access to their earnings.