Your payment infrastructure is product, and at scale, how it performs determines whether payees stay or leave. Payment operations is the function that determines whether your disbursement cycles run cleanly or break under volume. For platforms processing thousands of payments per cycle across ACH, wire, RTP, and international rails, the difference between a payment operations setup that holds and one that doesn’t comes down to infrastructure decisions made before the pressure hits. Failed payouts, reconciliation backlogs, compliance gaps, and rising support costs are the symptoms of a payment operations setup that hasn’t been built for scale.

TLDR:

- Payment operations covers three layers: execution across ACH, wire, RTP, and international rails; tax compliance and payee onboarding; and reconciliation. A gap in any layer breaks the whole cycle.

- Manual workflows fail somewhere in the hundreds of disbursements. At 5,000 per month, a 2% failure rate is 100 payments needing manual remediation per cycle.

- Three KPIs signal whether your infrastructure holds: payment success rate, days to fund, and exception rate. Failure above 2% points to data quality or routing problems.

- Automate scheduling, W-8/W-9 collection, tax tracking, ERP reconciliation, and sanctions screening to grow volume without adding headcount.

- If backlogs and exception queues are already growing, the fix is infrastructure decisions made before volume forces the issue.

What Is Payment Operations?

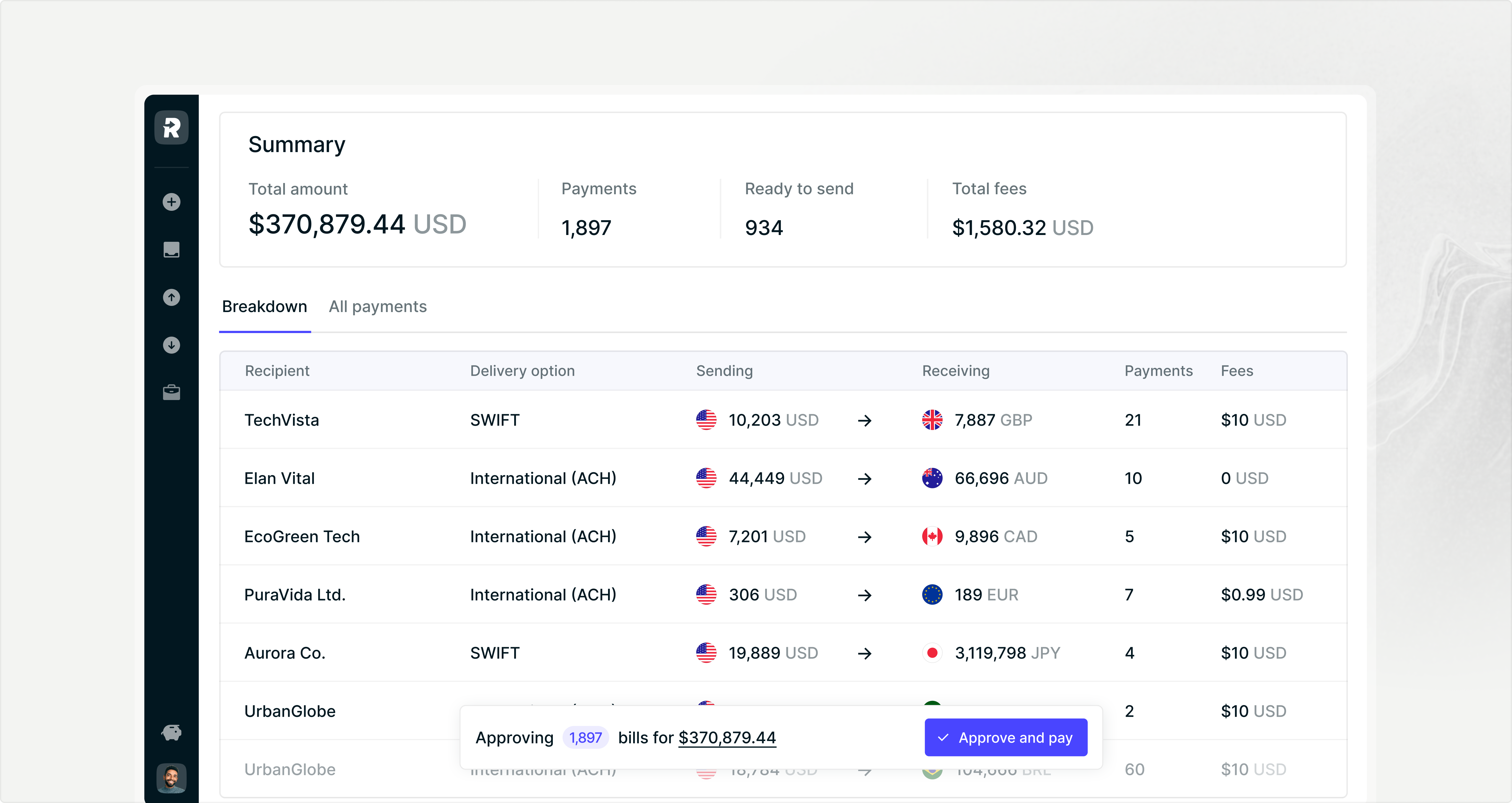

Payment operations is the end-to-end function responsible for executing, monitoring, and reconciling the movement of money across a business. For high-volume operators, that means managing the full lifecycle of every disbursement: initiating payouts, validating payee data, routing payments across rails like ACH, wire, or RTP, and confirming settlement on the other side.

At scale, this goes well beyond sending money. When you’re running thousands of payouts per cycle to creators, drivers, or gig workers across multiple countries, payment operations becomes the infrastructure layer that controls whether those payments land correctly, on time, and in compliance with tax and regulatory requirements.

The function typically spans three areas:

- Execution: Initiating and routing payments through the right rails based on speed, cost, and payee location, whether that’s domestic ACH or an international wire to a contractor in a different currency.

- Compliance and controls: Collecting W-8 and W-9s, screening payees against OFAC and sanctions lists, and generating 1042-S/1099-NEC forms at year-end without manual intervention.

- Reconciliation and visibility: Matching disbursements to source records, flagging failures, and giving finance teams real-time status across every payment in the cycle.

Where this breaks down is at volume. A manual process that works for 50 payouts a month becomes a liability at 5,000. Missed validations, inconsistent routing, and delayed reconciliation stop being process gaps and start being compliance exposures and payee churn risks.

Key Components of Payment Operations Infrastructure

For many teams, somewhere in the hundreds of monthly disbursements is where bank portals stop being workable. Past that point, manual routing decisions, exception handling, and reconciliation create compounding errors that no spreadsheet can absorb.

Four components make up the infrastructure stack you actually need:

- Payment rails: ACH for domestic batch disbursements, wire for high-value or urgent transfers, RTP/FedNow for instant 24/7 payouts, and local or SWIFT rails for international payees

- Routing logic: Rules that select the right rail based on payee location, currency, required arrival speed, and transaction cost

- API connectivity: Programmatic triggering, monitoring, and cancellation of payments without manual portal intervention per transaction

- Payee data layer: Validated banking details, tax form status, and sanctions screening results accessible at execution time

These components depend on each other. Routing logic without validated payee data produces failed disbursements. API connectivity without proper routing produces costly mis-routed payments. At volume, a gap in any layer creates cascading failures, not isolated ones. Payment operations infrastructure best practices focus on building integrated systems instead of point solutions.

Payment Operations Metrics and KPIs

At scale, small percentage-point swings in these numbers translate to thousands of dollars in failed disbursements, IRS penalties, or remediation costs, and direct payee churn.

Core KPIs to Monitor

- Payment success rate: The percentage of disbursements that clear without failure or return. For high-volume payout programs, persistent failure rates above 2% are generally treated as a signal of data quality or routing problems that compound fast.

- Days to fund: How long payees wait from trigger event to settled funds, directly shaping retention across contractor and creator networks.

- Exception rate: How often payments require manual intervention, which is your clearest signal that automation coverage has gaps.

- Reconciliation cycle time: How quickly your team closes the books after a payout run. Longer cycles typically indicate integration debt between your payout system and your ERP.

- Compliance filing accuracy: The percentage of 1042-S/1099-NEC forms issued without TIN mismatches or threshold errors. IRS penalties start accumulating per form the moment errors slip through.

Challenges in Scaling Payment Operations

The same processes that work at low volume become liabilities as payment cycles grow. Here’s how each challenge changes shape when you cross from hundreds of disbursements per month to thousands:

The result is a team spending more time on exception handling than on the payment cycles themselves.

Payment Operations Automation

The core functions that benefit most from automation include:

- Payment scheduling and batch processing: Disbursements go out on time without requiring someone to manually trigger each run.

- Payee onboarding and W-8/W-9 collection: Removes the back-and-forth that slows down contractor activation at scale.

- Tax compliance tracking: Monitors payees across the full payment year so you know who crossed the reporting threshold before the filing deadline arrives.

- ERP and accounting reconciliation: Eliminates the manual matching that breaks down once payment volume exceeds what a spreadsheet can handle.

- Fraud screening and sanctions checks: Applied programmatically at the time of payment instead of as a post-hoc audit.

The shift from manual to automated payment operations is less about convenience and more about capacity. Automation absorbs volume increases without a proportional increase in execution overhead.

Best Practices for High-Volume Payment Operations

At high volume, the gap between a payment operation that holds and one that breaks often comes down to five or six structural decisions made before the pressure hits. Real-time disbursement capabilities have moved from competitive advantage to baseline expectation across gig and creator platforms.

- Batch by geography and currency: Pre-funding currency corridors for your busiest payee populations before funds leave your system cuts failed disbursements caused by FX shortfalls mid-cycle.

- Automate W-8/W-9 collection at onboarding: Collecting forms retroactively when adding hundreds of contractors monthly creates compliance backlogs that compound every pay cycle.

- Build exception handling into your workflow: Every payment cycle produces failures. How fast you identify, reroute, and resolve them controls whether one failed payment becomes a hundred.

- Separate approval logic from payment execution: Manual approval steps become chokepoints at scale. API-driven routing lets you encode approval rules programmatically so volume doesn’t require proportional headcount.

- Run payee validation before disbursement: Bank account verification and OFAC screening at the point of onboarding catches errors before they reach the payment rail, where remediation costs time and money.

The through-line across all of these is that high-volume payment operations require infrastructure decisions, not process adjustments. Manual intervention at any step creates a capacity ceiling, and volume will find it.

How Routable Powers Payment Operations for High-Volume Platforms

Routable is an API-first mass payment solution built for operators running thousands of programmatic payments per cycle, not a general-purpose tool retrofitted for scale.

When your payment cycle involves onboarding hundreds of new contractors monthly, collecting W-8 and W-9s, screening payees, and disbursing across multiple currencies, each manual touchpoint is a liability. Routable handles that at the infrastructure level.

- Batch scheduling: Disbursements go out across time zones when payees expect them, not when a queue clears.

- W-8/W-9 collection and TIN validation: Tax forms and taxpayer IDs are collected and verified automatically before any payment is issued.

- API-driven routing: Programmatic payout requests are routed without manual intervention, regardless of volume.

- Multi-currency disbursements: International contractor networks are paid in local currencies with pre-funding support to prevent FX shortfalls mid-cycle.

- 1042-S/1099-NEC output: Tax forms are generated directly from payment records, so year-end filing is tied to the data, not a separate reconciliation exercise.

Final Thoughts on Building Payment Operations Infrastructure

Your payment operations infrastructure determines whether your disbursements become a retention advantage or a churn driver. When you’re paying thousands of contractors, creators, or gig workers monthly, payees who wait days longer than expected, or miss a payment entirely, don’t stay. They take the next platform that pays faster and more reliably. The operators who scale without breaking are running API-first infrastructure that removes manual bottlenecks before volume forces the issue. If reconciliation backlogs and exception queues are already piling up at your current scale, see how Routable handles mass payouts.

FAQ

What is payment operations?

Payment operations is the end-to-end function responsible for executing, monitoring, and reconciling disbursements across a business. At scale, it spans three layers: payment execution across multiple rails (ACH, wire, RTP, international corridors), compliance and tax form management, and reconciliation against source records. For platforms paying thousands of contractors, creators, or gig workers monthly, payment operations is the infrastructure layer that determines whether those disbursements land correctly, on time, and in compliance.

What are the most important KPIs in payment operations?

The three KPIs that matter most at scale are payment success rate, days to fund, and exception rate. Payment success rate tracks how many disbursements clear without failure — persistent failure rates above 2% typically signal data quality or routing problems. Days to fund measures how long payees wait from trigger event to settled funds, which directly affects retention across contractor and creator networks. Exception rate tells you how often payments require manual intervention, which is the clearest signal that automation coverage has gaps.

At what volume does manual payment processing break down?

Most teams hit the limit of manual processes somewhere in the hundreds of monthly disbursements. Past that threshold, manual routing decisions, exception handling, and reconciliation create compounding errors that spreadsheets cannot absorb. At 5,000 disbursements per month, a 2% failure rate means 100 payments requiring manual remediation per cycle. That is when bank portals and manual workflows stop being workable and start being a liability.

What payment rails should high-volume platforms support?

High-volume platforms typically need ACH for domestic batch disbursements, wire for high-value or urgent transfers, RTP/FedNow for instant 24/7 payouts, and local or SWIFT rails for international payees. The right rail depends on payee location, currency, required arrival speed, and transaction cost. Routing logic that selects the correct rail automatically, without requiring manual decisions per payment, is what separates a system that scales from one that does not.

How does automation change payment operations at scale?

Automation changes payment operations from a capacity-limited process to a volume-absorbing system. When payment scheduling, W-8/W-9 collection, tax compliance tracking, reconciliation, and sanctions screening are handled programmatically, volume can grow without proportional increases in headcount or error rate. The shift from manual to automated payment operations is less about convenience and more about removing the ceiling on how many disbursements your team can handle per cycle.

What is the difference between payment operations and accounts payable?

Payment operations and accounts payable overlap but serve different functions. Accounts payable typically covers invoice receipt, review, and approval: a workflow built around responding to incoming obligations. Payment operations covers outbound disbursement execution at volume: routing thousands of payments across multiple rails, managing payee compliance, and reconciling at scale. For platforms paying contractors, creators, and gig workers, the disbursement-first model of payment operations is the right frame, not the invoice-centric model of traditional AP.