Your drivers, creators, and sellers don’t compare your platform’s settlement speed against yesterday’s ACH window. They compare it against every faster-paying competitor actively recruiting them. Instant-to-card gets funds to a debit card in minutes, closing that retention gap, but the finality of card network settlement changes the infrastructure requirements around every disbursement. There is no return window. No reversal process. No recovery path after funds clear a card. For platforms running mass payouts to debit cards at scale, that permanence turns pre-send validation, compliance controls, and reconciliation logic from preflight checklists into structural requirements. At thousands of disbursements per cycle, a missed check before settlement is an unrecoverable loss, not a correctable error.

TLDR:

- Instant-to-card settles funds to a debit card in minutes, but there is no recovery path after settlement.

- Pre-send validation and OFAC screening are structural requirements on an irreversible rail, not optional checks.

- Running instant-to-card alongside RTP/FedNow manages cost and coverage gaps a card-only strategy creates.

- Charging a modest instant-access fee turns your disbursement infrastructure into a revenue line, not overhead.

- Routable handles multi-rail mass payouts via API or CSV with idempotency key support on every payout endpoint.

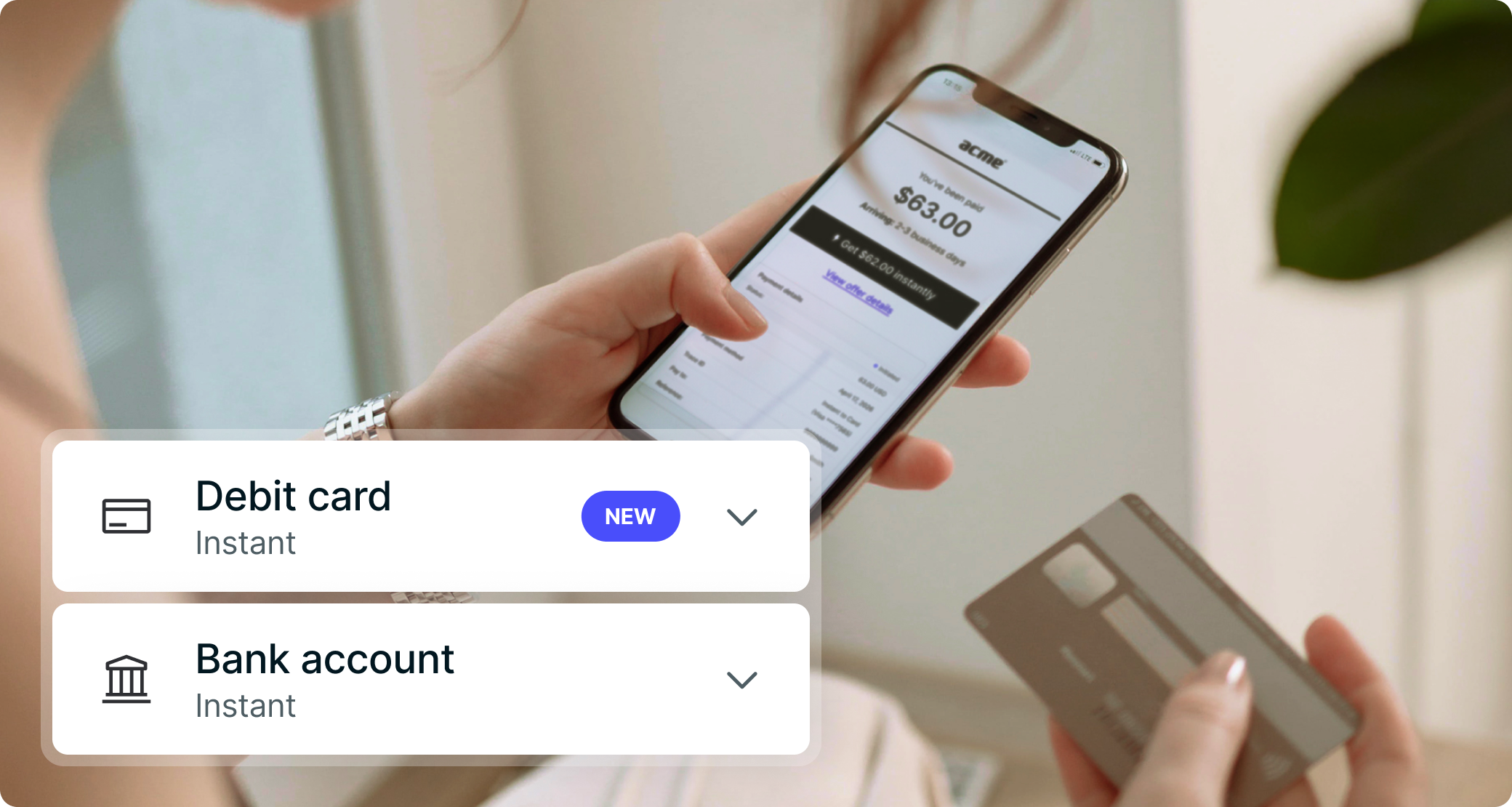

What Are Mass Payouts to Debit Cards?

Mass payouts to debit cards mean sending funds simultaneously to hundreds or thousands of debit card holders through card network rails, bypassing the ACH banking system entirely. Where ACH routes through bank account numbers and routing numbers, instant-to-card routes through the card networks directly to a debit card, settling in minutes instead of days.

The practical difference matters at scale. When a gig platform needs to pay 5,000 drivers at end of shift, or a marketplace needs to clear creator earnings on demand, waiting three to five business days for standard ACH settlement is a retention problem. Mass payouts at scale require a faster approach. Payees who can’t access earnings quickly start comparing competitors who pay faster.

How the Instant-to-Card Mechanism Works

When a payout is initiated over the instant-to-card rail, four discrete steps fire in sequence.

- Card network validation. The destination debit card is checked for active status and push-eligibility at the issuing bank before any funds move.

- Fraud screening. The payee record and transaction parameters run through fraud checks. Any flag at this stage stops the disbursement before settlement.

- Rail routing. Routing resolves across Visa Direct or Mastercard Send to identify the fastest available path to the destination card.

- Fund push. Funds push directly to the debit card, typically settling in minutes instead of days with no return window after completion.

Common Use Cases for Instant-to-Card Mass Payouts

Platforms across industries are turning to instant-to-card as their default disbursement rail precisely because of where their payees are. Most gig workers, creators, and independent contractors already have a debit card in their wallet. No new account setup, no ACH enrollment, no waiting for bank routing details to clear compliance checks.

Here are the use cases where instant-to-card mass payouts perform best:

- On-demand payouts for gig workers: platforms paying drivers and delivery workers after each shift find that near-immediate debit card settlement removes the biggest friction point between task completion and payment receipt, which directly affects whether workers accept the next job on your platform.

- Nonprofit grant disbursements: organizations distributing grant funds or disaster relief payments to recipients can replace check and ACH workflows with instant-to-card, getting funds to debit cards in minutes and reducing the support burden from recipients asking when payments will arrive.

- Creator economy payouts: creators treat payment speed as a platform quality signal, and on-demand disbursement to debit cards removes the friction that slow settlement creates.

- Seller payouts: offering instant payout as a premium tier after order fulfillment converts disbursement infrastructure into a revenue line, not a cost center.

- Earned wage and loan disbursements: lending and fintech companies distributing approved loan funds or earned wage advances need settlement speed that matches borrower expectations. Instant-to-card delivers funds in minutes versus the one to three business days standard ACH requires.

The common thread across all of these: payees are individuals, settlement speed matters to retention, and the debit card is already in hand.

Fee Structure and Cost Considerations

The instant-to-card vs. ACH cost comparison matters: instant-to-card costs more per transaction than standard ACH, and that difference compounds fast at scale. Because card networks do not publicly standardize fees, costs vary by provider. Industry estimates typically place interchange in the range of 1 to 3% per transaction, though your actual rate depends on your processor, volume tier, and card type.

For most platforms, that fee differential is worth it. When payees are contractors, gig workers, or creators who depend on timely access to earnings, the cost of slow settlement shows up in churn metrics before it shows up in a finance review. A modest instant-access fee charged to payees opting into instant-to-card turns that infrastructure cost into a revenue line, not overhead.

Running instant-to-card alongside RTP and FedNow manages the cost differential at scale, RTP and FedNow settle to bank accounts in seconds with flat-fee pricing commonly under $1.00, and together they cover more than 85% of U.S. bank accounts, so routing card-preferring payees to instant-to-card and bank-preferring payees to RTP/FedNow closes the coverage gap a card-only strategy creates. Whether you pass the instant-access fee to payees as a premium tier or absorb it as a retention investment, the economics only hold at volume: at a few hundred transactions a month the per-transaction premium is hard to defend, but at thousands the retention math moves in favor of instant rails.

Geographic Coverage and Card Eligibility Constraints

Instant-to-card payouts work across a wide range of countries, but geographic coverage varies by card network and provider. Visa Direct operates in over 195+ countries, while Mastercard Move reaches more than 200 countries. That gap matters when you’re running a global contractor network or disbursing grants across multiple regions. A rail that covers your primary corridors today may leave you without a path in secondary markets.

Eligibility also depends on the card type. Instant-to-card requires a debit card linked to a demand deposit account. Prepaid cards may work depending on issuer configuration, but credit cards are generally not supported on push rails.

Before committing to a instant-to-card strategy at scale, verify coverage for every payee corridor in your network. Your payout infrastructure for platforms needs to account for these gaps.

Compliance and Fraud Controls for Mass Card Disbursements

Paying thousands of contractors or gig workers via debit card introduces compliance exposure that scales with every transaction. Before a single dollar moves, your disbursement infrastructure needs controls that fire automatically, not checklists a human runs through before batch release.

Three control layers matter most at volume:

- OFAC screening: every payee record must be screened before funds are released. For platforms disbursing across state lines or to international debit accounts, a missed OFAC hit isn’t a filing error. It’s a regulatory violation with penalties that compound per transaction.

- Pre-send validation: catches stale or invalid card credentials, confirms payout amounts match the verified payee record, and flags any discrepancy before an instant-to-card attempt settles. Unlike ACH, which allows returns within a defined window, instant-to-card settles immediately and finally. There is no recovery path after funds hit a card, which means validation is the last and only line of defense before disbursement becomes unrecoverable.

- Payment orchestration: handles duplicate payment detection via idempotency keys, preventing network timeouts from producing double disbursements across a batch. At 10,000 transactions per cycle, a single retry loop without idempotency protection can corrupt your reconciliation ledger for the entire run.

Fraud patterns specific to instant-to-card include fake payee account injection, card credential substitution mid-cycle, and payment rerouting via compromised onboarding flows. Platforms running high-volume card disbursements should treat payee verification at onboarding, not at payout, as the primary fraud gate.

What to Look for in a Mass Payout Provider

When selecting a mass payout provider, the rail menu matters less than whether those rails connect through a single stack. Look for these capabilities:

- Multi-rail coverage: instant-to-card, RTP/FedNow, ACH, and international rails accessible through one payouts API for disbursements without separate integrations per method

- Self-serve payee onboarding: collects card or bank details without per-payee engineering work on your side

- Native compliance: sanctions screening, KYC, and TIN validation built directly into the disbursement layer, not added separately

- CSV and API ingestion paths: operations teams can run batches immediately while engineering automates later

- Idempotency key support: every payout endpoint blocks duplicate payments during network retries

- Real-time ERP sync: surfaces payment status without manual reconciliation steps after each run

Any gap in this list becomes a manual exception process. At thousands of payouts per cycle, exceptions don’t get resolved cleanly. They accumulate.

How Routable Handles Multi-Rail Mass Payouts at Scale

Routable handles the full disbursement stack via REST API or CSV batch upload, validation, compliance screening, rail selection, and settlement without manual intervention, across ACH (four speed tiers), RTP/FedNow, wire, check, and international transfers to 220+ countries and territories in 140+ currencies, with idempotency key support on every payout endpoint and fallback routing when a primary rail fails. White-label onboarding collects W-8/W-9s and payment preferences through a custom-branded interface, with bank account ownership verification and TIN validation running at onboarding so compliance is finished before a payment triggers. Routable’s bi-directional ERP sync with Oracle NetSuite, Sage Intacct, QuickBooks Online, and Xero records payment status and multi-currency values back into the general ledger at 99.8% accuracy, with no manual reconciliation steps after each run.

A few capabilities worth noting for teams running mass payouts to debit cards at scale:

- Pre-send validation: checks payee details before funds move, which is the last line of defense on an irreversible rail. There is no recovery path after instant-to-card settles, so catching errors before disbursement is structural, not optional.

- Batch processing: handles high volumes programmatically, so a payment run of 5,000 or 50,000 doesn’t require proportionally more overhead.

- Multi-rail routing: lets payees receive funds via their preferred method without requiring you to manage separate workflows per rail.

- Real-time status visibility: surfaces payment state across your entire batch, so your support team isn’t fielding “where’s my payment” questions they can’t answer.

- Compliance automation: handles W-8/W-9 collection and flags payees who cross the reporting threshold, keeping tax documentation from becoming a bottleneck at volume.

Final Thoughts on Scaling Mass Payouts to Debit Cards

Instant-to-card solves the settlement gap, but it also raises the stakes on everything upstream. With no return window after funds clear, your validation and compliance controls carry all the weight. Getting the rail right matters, but getting the infrastructure around it right is what keeps a payout operation from producing unrecoverable losses at scale. If your current setup wasn’t built for that kind of finality, talk to Routable.

FAQ

What’s the difference between instant-to-card and RTP/FedNow for mass payouts to debit cards?

Instant-to-card routes funds through Visa Direct or Mastercard Send directly to a debit card, settling in minutes but requiring an eligible debit card and carrying percentage-based fees typically estimated between 1 and 3% per transaction. RTP and FedNow settle directly to bank accounts in seconds, 24/7/365, with flat-fee pricing commonly under $1.00 per transaction and no card eligibility requirement. For platforms running mass payouts to debit cards at scale, the right answer is usually both rails running in parallel: instant-to-card for payees who want card delivery, RTP/FedNow for everyone else, with ACH as the fallback for accounts not yet on a real-time rail.

Can I run mass payouts to debit cards without rebuilding my existing ACH disbursement infrastructure?

Bolting instant-to-card onto ACH-native infrastructure without rebuilding the validation, compliance, and reconciliation layers underneath it is the default failure mode at volume. Instant-to-card settles immediately and finally with no return window, so pre-send payee validation becomes a structural requirement, not a preflight checklist. Reconciliation logic built for batch ACH breaks when applied to real-time card disbursements because settlement timing, fee structures, and failure codes are categorically different. Platforms that add instant-to-card as a rail without rebuilding these layers encounter the gaps under load, not during testing.

How do idempotency keys prevent duplicate payments in high-volume debit card disbursement batches?

An idempotency key is a unique identifier attached to each payout request that tells the system to treat any retry of that request as the same transaction, not a new one. Without idempotency key support on every payout endpoint, a network timeout during a 10,000-payment batch does not produce one failed transaction. It produces undetectable duplicates that corrupt your reconciliation ledger for the entire cycle, and on an instant-to-card rail with no recovery path after settlement, those duplicates are unrecoverable losses.

What OFAC and compliance controls should I have in place before running mass payouts to debit cards?

OFAC screening must run against every payee record before funds are released. On an instant-to-card rail where settlement is immediate and final, a missed OFAC hit is a regulatory violation compounding per transaction, not a filing error you can correct after the fact. Pre-send validation checking that each debit card is active and push-eligible, fraud screening against the payee record and transaction amount, and duplicate payment detection via idempotency keys are the three control layers that matter most at volume. Platforms running high-volume card disbursements should treat payee verification at onboarding as the primary fraud gate, not a step that fires at payout.

When does instant-to-card stop making economic sense compared to RTP/FedNow for gig platform payouts?

Instant-to-card carries estimated interchange costs in the 1-3% range per transaction plus a minimum floor around $1.00, $1.50 on smaller payouts, while RTP and FedNow typically use flat-fee pricing under $1.00 per transaction. For platforms disbursing large volumes of small-value payouts (a gig driver earning $18 per shift, for example), the minimum fee on instant-to-card can exceed the percentage-based calculation and compress the economics fast. The point where instant-to-card fees become harder to defend relative to RTP/FedNow depends on your average payout size, volume tier, and whether you are passing the instant-access fee to payees as a premium tier or absorbing it as a retention investment.