Your platform already pays thousands of vendors every month. But when a contractor finishes a Friday shift and sees four-day ACH settlement, they open the app that pays instantly. Speed is the most visible part of payout infrastructure for platforms, and it’s the first thing payees judge you on. Around 1,000 monthly disbursements, the manual workflows that got you here start to fail. Missing routing numbers stall entire batches. Tax forms pile up unvalidated. Reconciliation drifts until close. If you’re scaling from hundreds to thousands of payees, you need infrastructure built for execution at volume, not AP tooling retrofitted for mass payouts.

TLDR:

- At 1,000+ monthly disbursements, manual workflows break: you need payout infrastructure, not AP tooling.

- Payout speed is a retention lever: 84% of gig workers rank fast earnings above incremental pay differences when choosing a platform.

- Multi-rail coverage (ACH, RTP, FedNow, SWIFT, local rails) is required to serve every payee type and region.

- Tax compliance (W-8/W-9 collection, TIN validation, 1099 filing) must automate as your payee network grows.

- API-first infrastructure lets you trigger payments on event completion and scale without adding headcount.

What Payout Infrastructure for Platforms Actually Means

Payout infrastructure is the set of rails, APIs, compliance checks, and reconciliation logic that moves money from your accounts to a large recipient network on a recurring, programmatic basis. It is not invoice intake or approval routing. You already know who to pay and when. The question is whether the system can execute at volume.

That line separates mass disbursement infrastructure from AP tooling. AP software receives and reviews invoices before payment. Payout infrastructure assumes the calculation already happened inside your product, and the job is execution: thousands of creator, driver, seller, or grantee payments routed through the right rail, with the right tax treatment, on schedule.

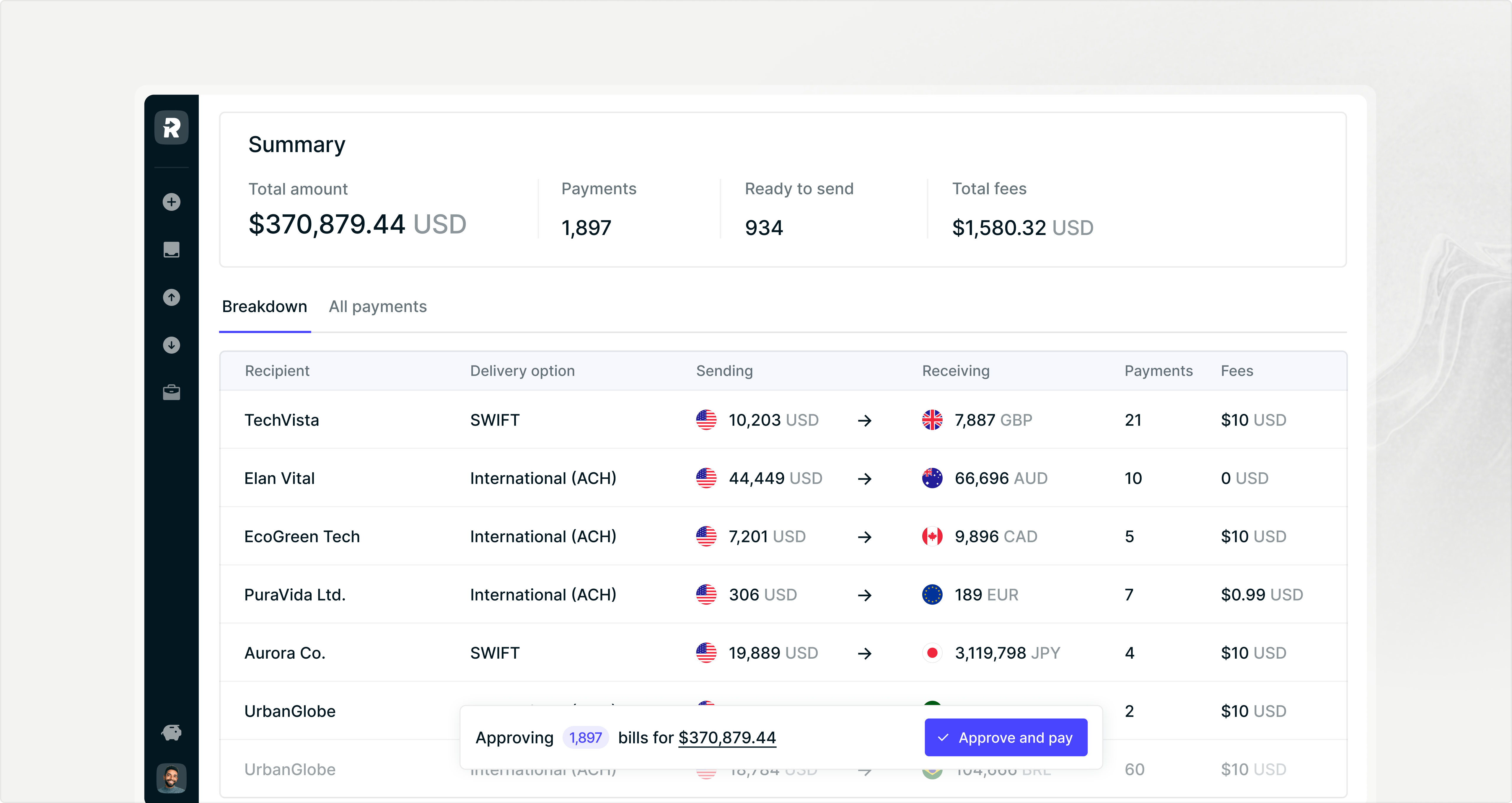

Manual portals and spreadsheets hold up to a few hundred payouts monthly. Around 1,000 disbursements, failed routing numbers, missing tax forms, and reconciliation drift surface at once. At that volume, you need infrastructure, not a CSV held together by one operations hire.

Why Speed Determines Payout Infrastructure Performance

Speed is the most visible part of your payout infrastructure, and the one payees judge first. 84% of gig workers say fast access to earnings is important or very important when choosing a platform, ranking payout speed on par with base pay and job availability. When a driver finishes a Friday shift, a four-day ACH settlement is a reason to open a competing app.

Rail choice makes that promise real. Standard ACH typically settles in four to five business days. Same Day ACH lands by 6pm ET. RTP and FedNow clear in seconds, 24/7/365.

U.S. real-time payment volumes are projected to reach 8 billion in 2026, growing above 30% annually. Instant payouts are the floor your payees compare you against.

Payment Rails Your Infrastructure Must Support

Different payouts demand different rails. A $40 driver tip and a $12,000 international grant should not move the same way. Infrastructure has to carry every option and route to the right one based on payee location, urgency, cost, and method preference.

The harder part is the routing logic on top. Your system needs to know that a U.S. driver with an RTP-eligible bank gets instant settlement, a contractor in Argentina gets local rails in pesos, and a payee missing bank details falls back to check without manual triage.

Tax Compliance Automation at Scale

Tax compliance is where payout volume turns into legal exposure. As payee networks double year over year and the US freelance workforce reaches 76.4 million, manual W-8/W-9 collection collapses before year-end filing.

Infrastructure has to handle four jobs in the background:

- W-8/W-9 Collection: Gather tax forms during payee onboarding, before the first payout clears

- TIN Validation: Match TINs against IRS records to catch mismatches before filing

- Threshold Tracking: Monitor cumulative payments per payee against current reporting thresholds

- Year-End Filing: Generate and file 1099-NEC, 1099-MISC, and 1042-S forms at year-end

The hard part is sorting payees correctly. International contributors need 1042-S treatment with treaty-based withholding applied at payment time. Domestic contractors need 1099 routing. A system that cannot tell them apart pushes that work onto your finance team every January.

API-First Architecture vs CSV Batch Processing

Two methods drive most payouts: CSV batch uploads and API integration.

- CSV Uploads: Finance teams launch high-volume payouts on day one without engineering effort. Export, map fields once, process thousands per batch.

- API Integration: Unlocks event-driven payouts: a tournament ends, a ride completes, a grant gets approved, and the payment fires automatically.

The graduation path matters more than the starting point. Ad-hoc bonus runs and corrections stay on CSV while recurring high-frequency payouts move to the API.

Cross-Border Disbursement Complexity

International payments compound every problem domestic ones already have. Each transaction clears sanctions screening, country-specific bank field validation, and FX conversion before funds move.

Your infrastructure has to handle three layers at once:

- Sanctions Screening: Screen every payee against 6,000+ watchlists (OFAC, EU, FTO) at onboarding and pre-payment

- Bank Field Validation: Validate IBANs, SWIFT codes, and local account formats that differ by country

- Rail Routing: Route through SWIFT or local rails based on cost, speed, and recipient currency

When regional banks go offline or sanctions shift overnight, automated rails stall. Paying journalists in South Asia or grantees in unstable regions sometimes requires manually rerouting funds through alternate corridors, which a fully automated provider cannot do without human intervention.

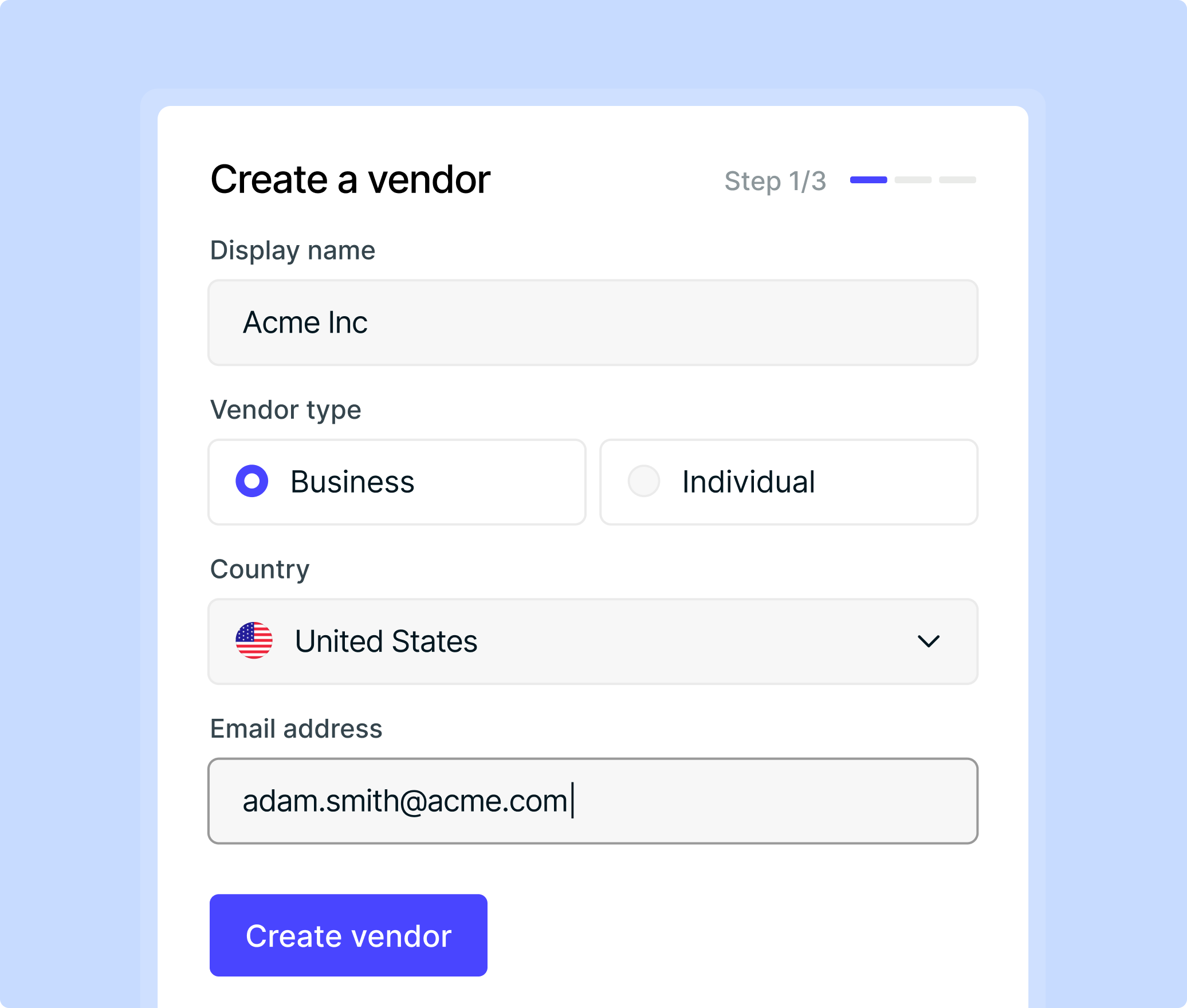

Payee Onboarding Experience as Infrastructure

Onboarding decides whether a payee ever gets paid. A driver who finishes their first shift and hits a generic third-party portal asking for routing numbers, a W-9, and ID verification will close the tab. That dropout becomes a support ticket, then churn.

Treat onboarding as infrastructure that runs continuously:

- Branded Self-Service Collection: Gather bank details and W-8/W-9s under your brand, 24/7, without routing payees to a generic third-party portal

- Bank Ownership Validation: Confirm account ownership via Plaid or micro-deposits to catch wrong account numbers before the first transfer

- TIN Matching: Verify TINs against IRS records at signup, not year-end, so mismatches surface before they become filing problems

- Sanctions Screening: Screen payees at onboarding so flagged individuals never reach payment status

Done well, time-to-first-payment drops from days to minutes.

ERP Integration and Reconciliation Requirements

Every payout creates an accounting event. If your general ledger does not see it within minutes, finance spends the last week of each month matching bank statements to disbursement reports by hand.

Bi-directional sync with NetSuite, Sage Intacct, QuickBooks Online, or Xero closes that gap. Bills, payments, payee records, and status changes move both ways, so an API-fired payout lands as a coded entry without a CSV export.

Four requirements matter at volume:

- Reference Field Mapping: ACH IDs and SWIFT IDs sync back to the original bill without manual matching

- Multi-Entity Routing: Payments route from the right subsidiary to the right GL automatically

- Custom Field Preservation: Class, department, program, or grant codes carry through every disbursement

- Sync Error Logs: Failed records surface with manual retry options so nothing drifts silently

Fund accounting teams feel this hardest. A grant disbursement that loses its program code forces a manual fix before close.

Scaling Challenges at Specific Volume Thresholds

Volume changes what breaks. The failure modes shift as your payee network grows, and infrastructure that worked at one tier becomes the bottleneck at the next.

The trigger is rarely one failure. It’s the week your ops lead spends three days reconciling a batch while support tickets pile up asking where Friday’s pay went.

How Routable Turns Payout Infrastructure into a Competitive Advantage

Routable is API-first payout infrastructure for operators who already know what to pay and need execution at volume. Teams process 10,000+ monthly payments without adding headcount, starting on CSV the same day and graduating to the API in under three developer days.

The pieces line up with what earlier sections require:

- Multi-Rail Coverage: Same Day ACH, RTP, and FedNow domestically; SWIFT and local rails across 220+ countries and 140+ currencies

- White-Labeled Onboarding: Collects W-8 and W-9s, validates TINs, and screens against 6,000+ watchlists under your brand

- Year-End Tax Filing: Generates and files 1099-NEC, 1099-MISC, and 1042-S with automatic domestic/foreign sorting

- ERP Sync: Bi-directional sync with NetSuite, Sage Intacct, QuickBooks Online, and Xero at 99.8% accuracy

- Manual Intervention: Reroutes payments for journalists and grantees in regions where automated rails stall

For platforms scaling from 500 creators to 50,000 gig workers, that combination turns payouts into a reason payees stay.

Final Thoughts on Building Payout Systems That Retain Payees

Payout infrastructure becomes a retention lever the moment your volume crosses 1,000 monthly disbursements. Payees compare your payment speed against every other option, and slower rails mean lost contractors, creators, and drivers to competitors who execute faster. The system you choose now decides whether your operations team reconciles spreadsheets or builds the business, and whether payees view your payments as reliable product or a reason to switch.

FAQ

When should a platform move from manual payouts to dedicated payout infrastructure?

Around 1,000 monthly disbursements is the practical threshold. Below that, spreadsheets and bank portals are painful but manageable. Above it, failed routing numbers stall entire batches, tax form collection falls behind, and reconciliation drift compounds before close. At that point, manual workflows cost more in ops time and error remediation than infrastructure does in fees.

What payment rails does payout infrastructure need to support?

At minimum: Standard ACH for low-urgency batch disbursements, Same Day ACH for weekly creator and contractor payouts, RTP and FedNow for shift-end gig worker payouts, wire for high-value transfers, and SWIFT plus local rails for international payees across 140+ currencies. The rail matters less than the routing logic on top. Your system needs to select the right rail automatically based on payee location, bank eligibility, urgency, and cost.

How does payout speed affect payee retention?

Directly. Research shows 84% of gig workers rank fast access to earnings as important or very important when choosing a platform, on par with base pay and job availability. A driver who finishes a Friday shift and sees a four-day ACH settlement has a concrete reason to open a competing app. Speed is the most visible part of your payout infrastructure and the first thing payees judge you on.

What tax compliance steps need to automate as payee volume grows?

Four jobs must run in the background without manual intervention: W-8/W-9 collection during payee onboarding, TIN validation against IRS records before filing, threshold tracking per payee against current reporting thresholds, and year-end generation and filing of 1099-NEC, 1099-MISC, and 1042-S forms. International payees require 1042-S treatment with treaty-based withholding applied at payment time. A system that cannot sort domestic from foreign payees pushes that work onto your finance team every January.

What is the difference between API-driven payouts and CSV batch processing?

CSV batch processing lets finance teams launch high-volume payouts without engineering effort: export a file, map fields once, process thousands per batch. API integration unlocks event-driven payouts where payment fires automatically when a trigger fires: a tournament ends, a ride completes, a grant gets approved. Both are valid approaches suited to different team structures and volumes. Most platforms start on CSV and move recurring, high-frequency payouts to the API as volume grows.